A stronger-than-expected indicates no rate cut before September despite the President’s demands. Nonetheless, households are becoming more pessimistic about employment prospects, with the risk of layoffs rising in the second half of the year.

Jobs Report Stronger than Expected

The June US jobs report shows nonfarm payrolls rising 147,000 versus the 106,000 consensus, with 16,000 of upward revisions to the past two months of data. Meanwhile, the surprisingly fell to 4.1% from 4.2% while the market was solidly backing the view that unemployment would actually tick higher to 4.3%.

President Trump has been calling for the Federal Reserve to cut the policy rate 200-300bp immediately, and two of his appointees (Chris Waller and Michelle Bowman) had suggested that they could vote for a rate cut as soon as this month’s FOMC meeting. But the rest of the FOMC is far more cautious, and today’s data indicates there will be no rate cut before the September FOMC meeting, especially with tariffs set to push inflation higher over the next few months.

")

Details are Less Rosy

Admittedly, the details are less positive with private payrolls rising only 74k versus expectations of a 100k gain. Government managed to post a 73k increase as a 47k increase in state government workers and a 33k increase in local government workers more than offset a 7k fall in the Federal government. Leisure and hospitality added 20k, and private education and healthcare services added 51k.

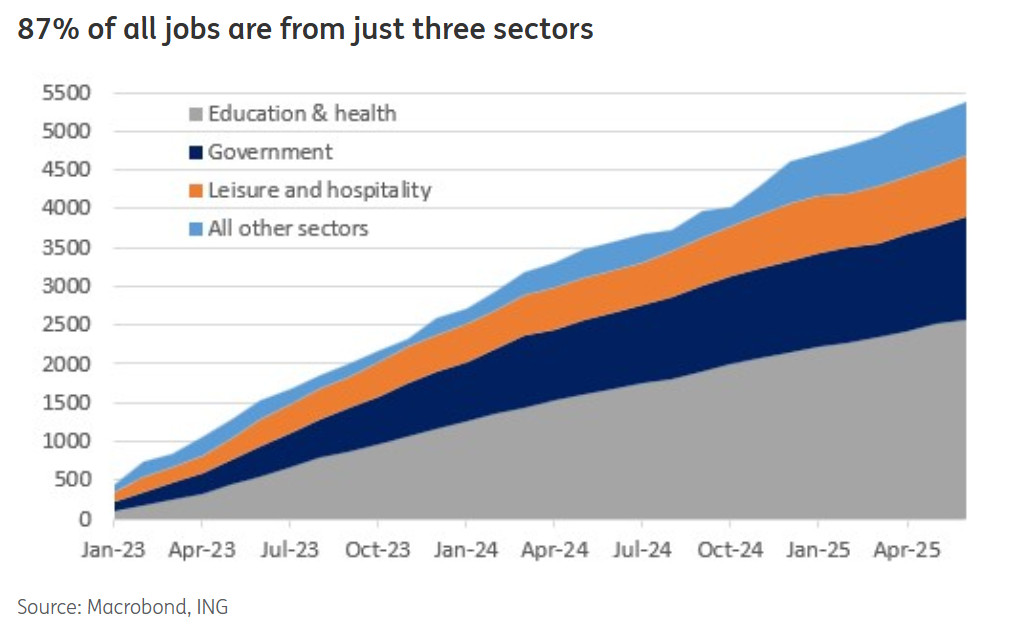

So the story is that these three sectors – government, leisure & hospitality, plus private education and healthcare services – have contributed 87% of all the jobs added in the past two-and-a-half years. The traditional sectors we would typically associate with a strong and vibrant economy are not adding jobs. We also note that wage growth was more subdued than expected, rising 0.2% month-on-month, while average hours worked per week fell to 34.2 from 34.3.

Trouble May Be Coming

Our suspicion is that government, private education & healthcare services, and leisure and hospitality will become much less supportive through the year and potentially even act as a drag on job creation later this year and into 2026.

Private healthcare jobs are vulnerable to the healthcare spending cuts that are part of President Trump’s One Big Beautiful Bill Act and if consumers do start to become more cautious in their spending, reflecting the steep falls in sentiment, then discretionary spending on eating and drinking in bars and restaurants and other entertainment tends to be the first thing that gets cut. We also expect to see Federal government workers shrinking as a legacy of Elon Musk’s efforts to get a grip on government spending.

Moreover, our sense that while hiring more broadly has been slowing as the economy loses some economic momentum, we are unlikely to see any meaningful job lay-offs is looking a little vulnerable to recent news flow. In particular the pick-up in Worker Adjustment and Retraining Notification notices, which requires most medium- and larger-sized employers to provide notification 60 calendar days in advance of planned closings and mass layoffs of employees, suggests that layoffs could rise from late summer onwards.

This tallies with the upward momentum in both initial and continuing jobless claims and the fact that the ISM employment numbers for both manufacturing and service sector firms have been in contraction territory in recent months.

Federal Reserve Set to Cut Rates in the Fourth Quarter

In terms of what this means for the Federal Reserve, most FOMC members are cautious, wanting to see what the tariff impact on inflation will be before acting in response to potential labour market weakness. This was certainly the tone adopted by Fed Chair Jerome Powell at last week’s appearances before Congress where he stated, “we are well positioned to wait to learn more about the likely course of the economy before considering any adjustments to our policy stance.”

With the uncertainty over inflation, the Fed would likely need to see clearer evidence of softness in the form of subdued payrolls growth and a rising unemployment rate to trigger an early move. Market pricing for the Fed this year has slipped from 67bp of cuts to 53bp in the wake of today’s report. We are sticking with our view of 50bp of rate cuts in the fourth quarter with a further 75bp of cuts in 2026.