Nikada/iStock Unreleased via Getty Images

Apple Inc. (NASDAQ:AAPL) is arguably one of the largest tech names in the world now. From the humble Apple-1, the company has expanded on a gargantuan scale, to a point where almost everyone owns an iPhone. Following the company’s expansion, we’ve seen AAPL stock rise hugely in valuation, almost hitting $200 a couple of months ago. However, the stock price has since pulled back pretty significantly, and currently sits at about $171 a share as of today. In this article, I explain why this valuation is an attractive one by analyzing the company’s fundamentals and financials, and then calculating a fair valuation of its stock price.

Apple – the benchmark for tech

It goes without saying that Apple has cemented itself as a major technological powerhouse, with many large tech companies using it as the benchmark for success. In fact, it is currently the largest tech company in the world by revenue, generating a whopping $394.33b in 2022. Warren Buffett swears by the company and invests heavily in it, to a point where it holds the largest stake in Berkshire Hathaway’s (BRK.A) equity portfolio. Other well-known heavy investors of AAPL stock are none other than BlackRock and The Vanguard Group – two of the world’s largest asset managers. Now, the confidence in the company is certainly not overstated. Let’s go over just how successful Apple really is as a company.

Products

One way Apple has consistently proven itself over the years is through its consistent rise in product adoption and sales. The company has managed to maintain a strong market presence across many of its products.

iPhone

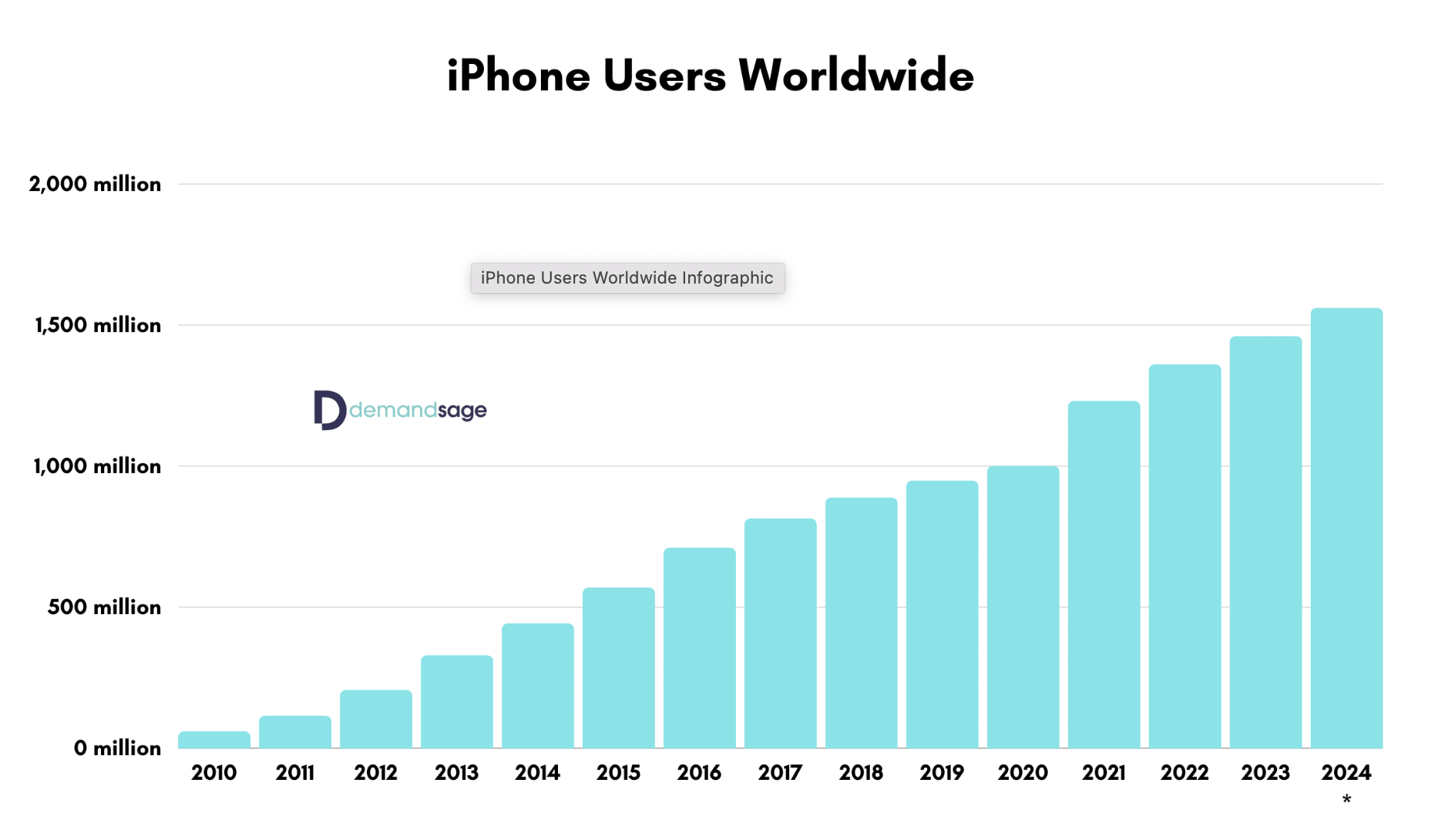

iPhone Users Worldwide (projected) (demandsage)

A glance at the chart provided by demandsage reveals a strong upward trend of iPhone users year-by-year. As of 2023, there are over 1.46b iPhone users, and we’re facing a projected number of over 1.5b users in 2024 – that’s almost 20% of the world that owns an iPhone. Over the past decade, this represents a total growth in users of over 44000%. The exponential growth in iPhone users over the past decade is immense.

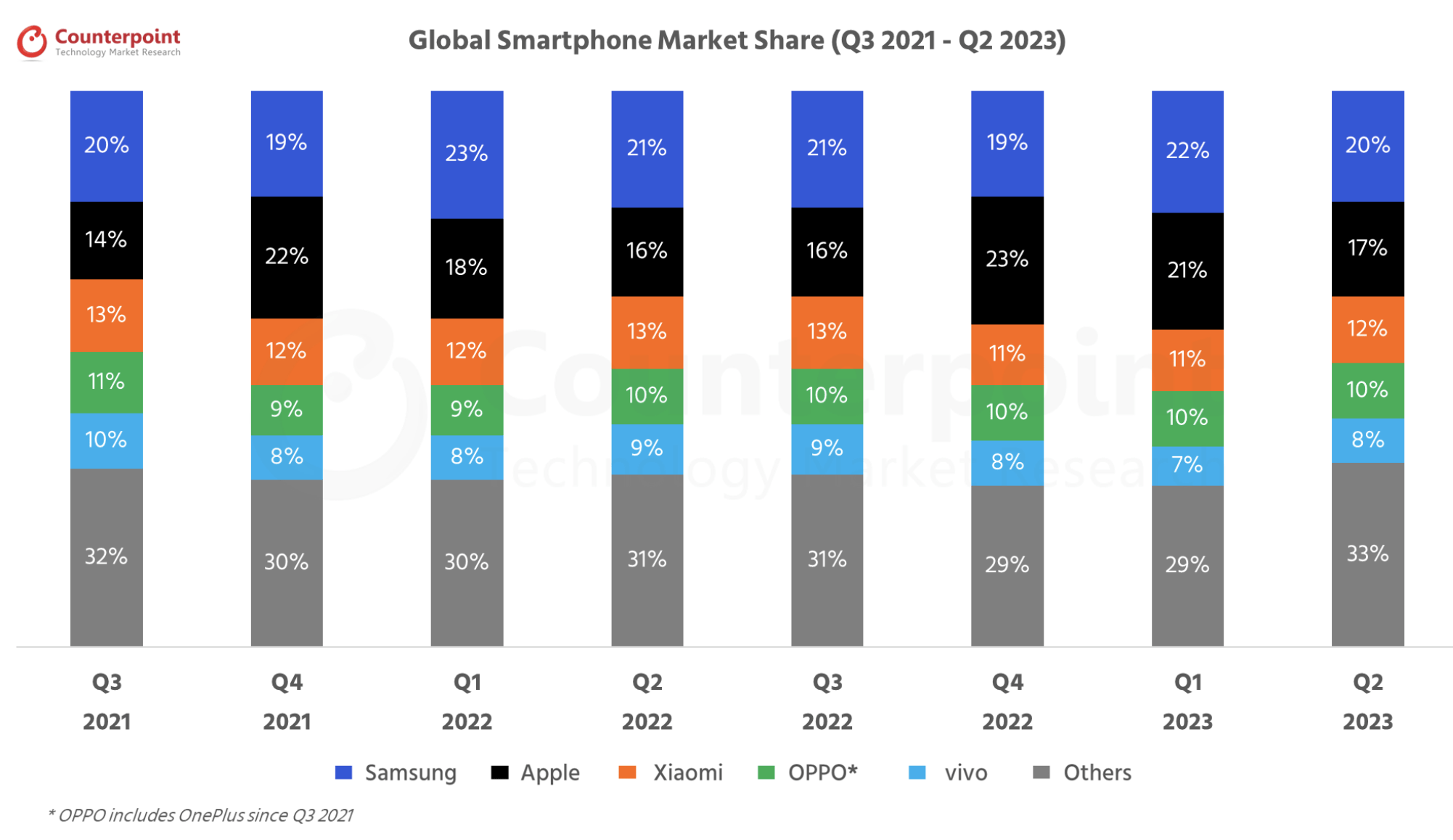

Global Smartphone Market Share (Q3 2021 – Q2 2023) (Counterpoint)

We also see in Counterpoint’s report that Apple still holds majority of the global smartphone market share, steadily hovering at about 30%. While the industry competition is definitely a cause for concern, it cannot be denied that Apple has definitely held its own for the past few years.

Computers

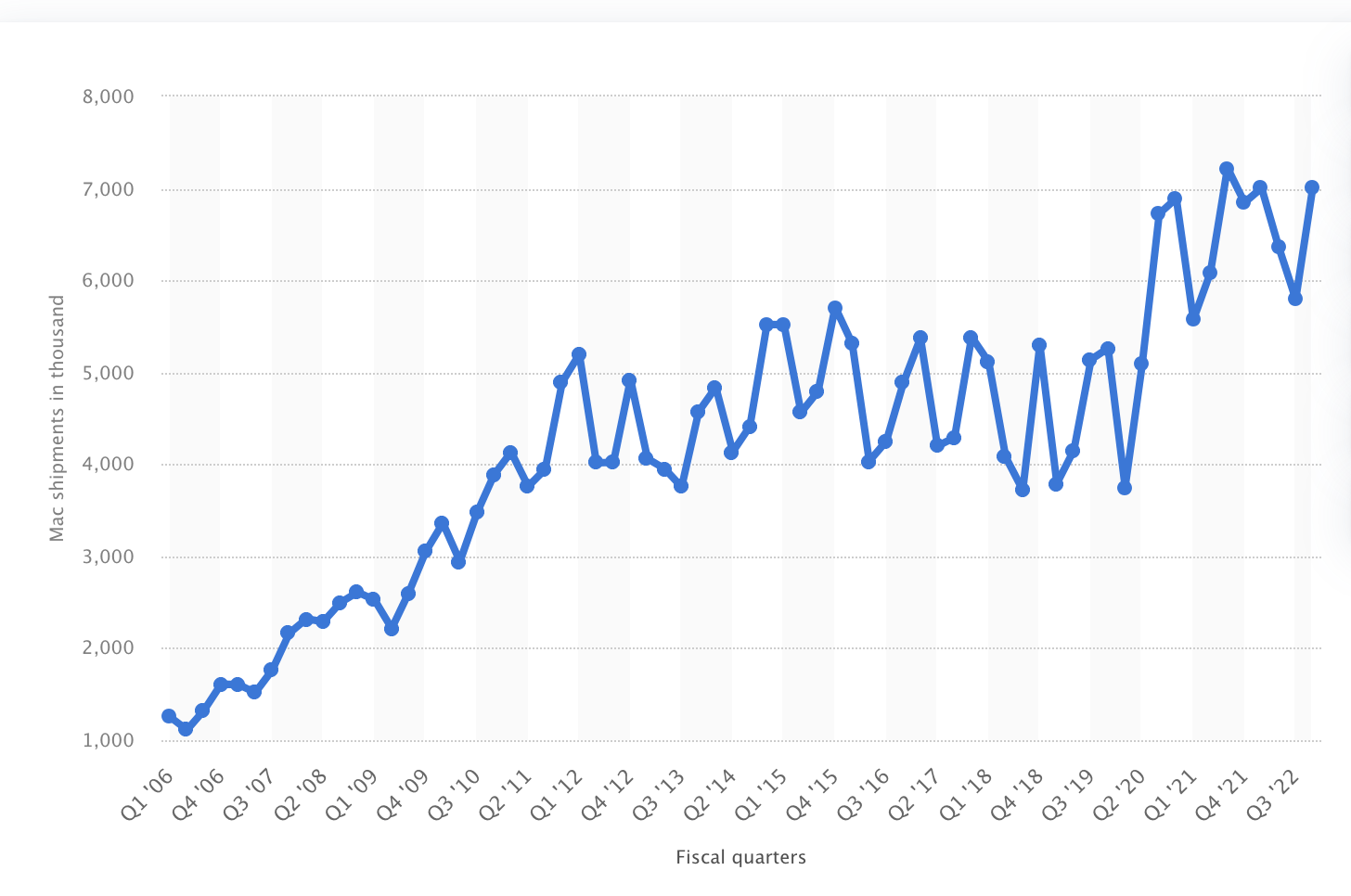

Global unit shipments of Apple Mac computers from 1st quarter 2006 to 4th quarter 2022 (Statista)

A rise in global unit shipments of Apple computers over the years also reflect an increasing adoption of Apple’s computer products. However, it is noteworthy that the trend in this case is not as strong, with fluctuations between quarters. We also see a bit of a dip from late 2015 to early 2020. However, the bounce back was strong in 2021, and computer shipments have been on a steady rising trend ever since. A rise in demand could be due to Apple’s new offerings in the iMac, which includes their in-house M1 chip and a new sleek exterior, coupled with larger consumption arising from a recovery from the Covid-19 pandemic.

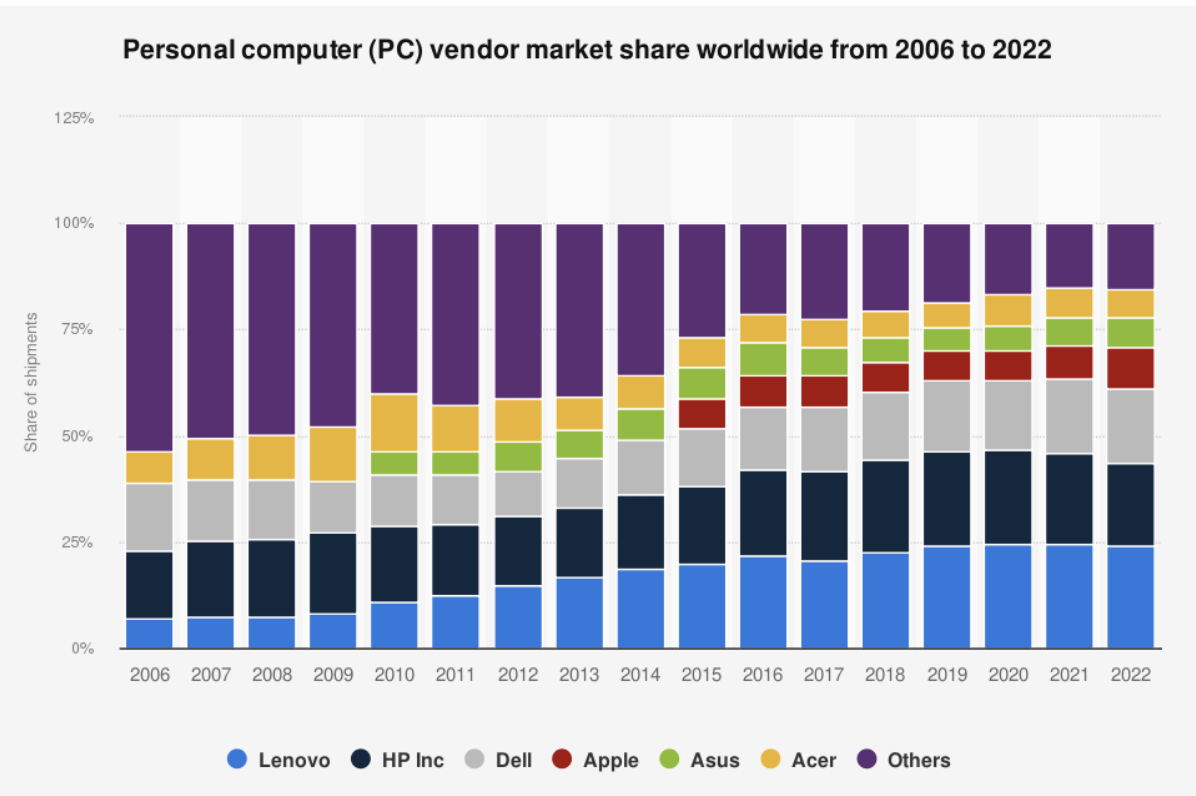

PC Vendor Market Share Worldwide (2006 – 2022) (Statista)

When it comes to market share, we see that Apple’s presence in the PC market has been steadily increasing since 2015. It’s clear that the adoption of the company’s PC offerings has been strong, rivalling the likes of Asus and Acer who have had a strong presence in the market since 2010.

AirPods

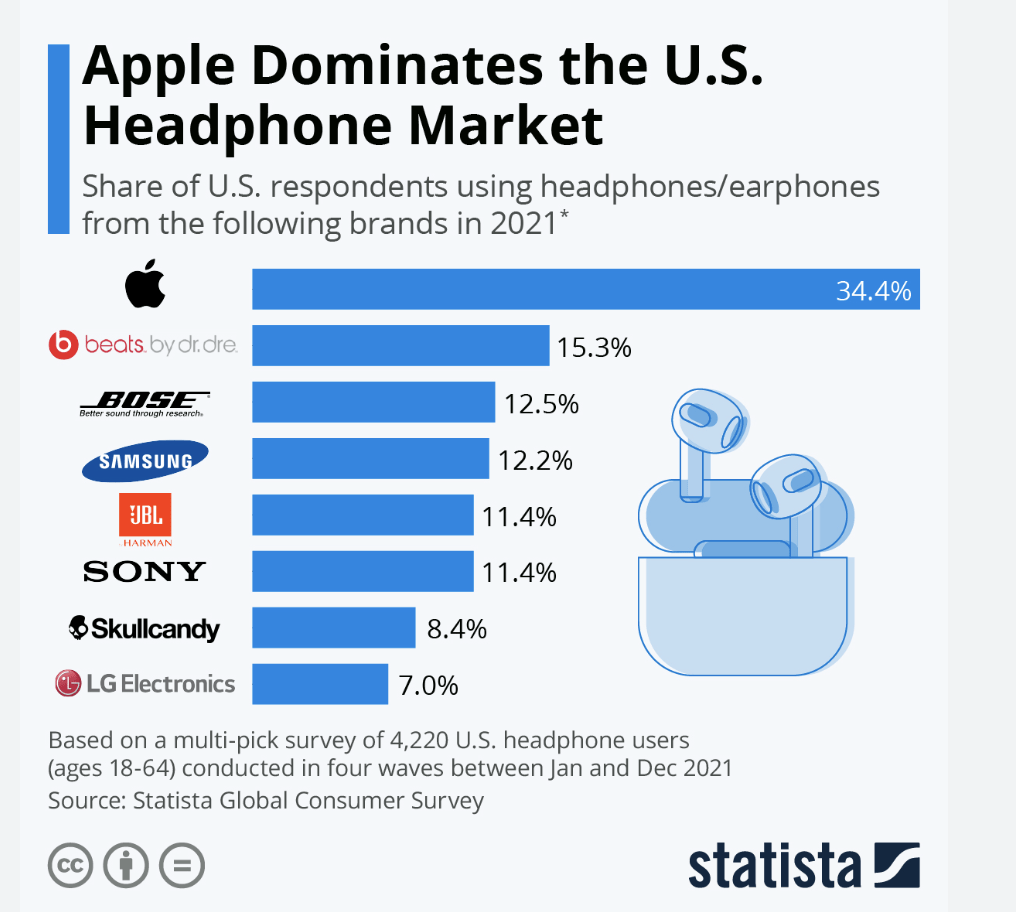

Share of US respondents using headphones/earphones (2021) (Statista)

The first launch of AirPods was in 2016. Since then, the product has taken the world by storm, and the adoption of the product has increased to a point where more than a third of participants in a multi-pick survey conducted by Statista were using them instead of other brands in 2021. We have to remember that the likes of BOSE, Sony, LG Electronics etc. have been in the businesses years before the AirPods were released, yet the AirPods still emerge superior.

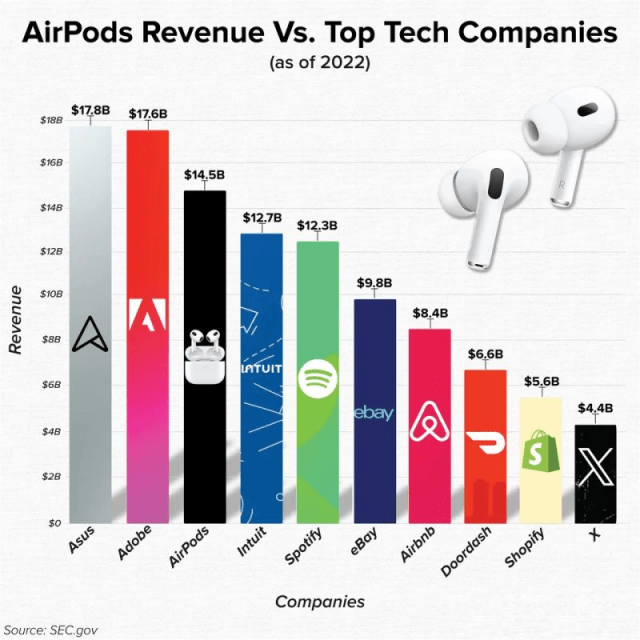

AirPods Revenue vs Top Tech Companies as of 2022 (SEC)

Here’s another interesting statistic about the AirPods. The chart above shows that Apple’s revenue generated from AirPods sales alone exceeds that of companies like Spotify (NYSE:SPOT), eBAY (NASDAQ:EBAY) and Shopify (NYSE:SHOP), just to name a few. This speaks volumes about not just the success of the product, but the sheer scale at which Apple is able to generate sales worldwide.

Strategic acquisitions

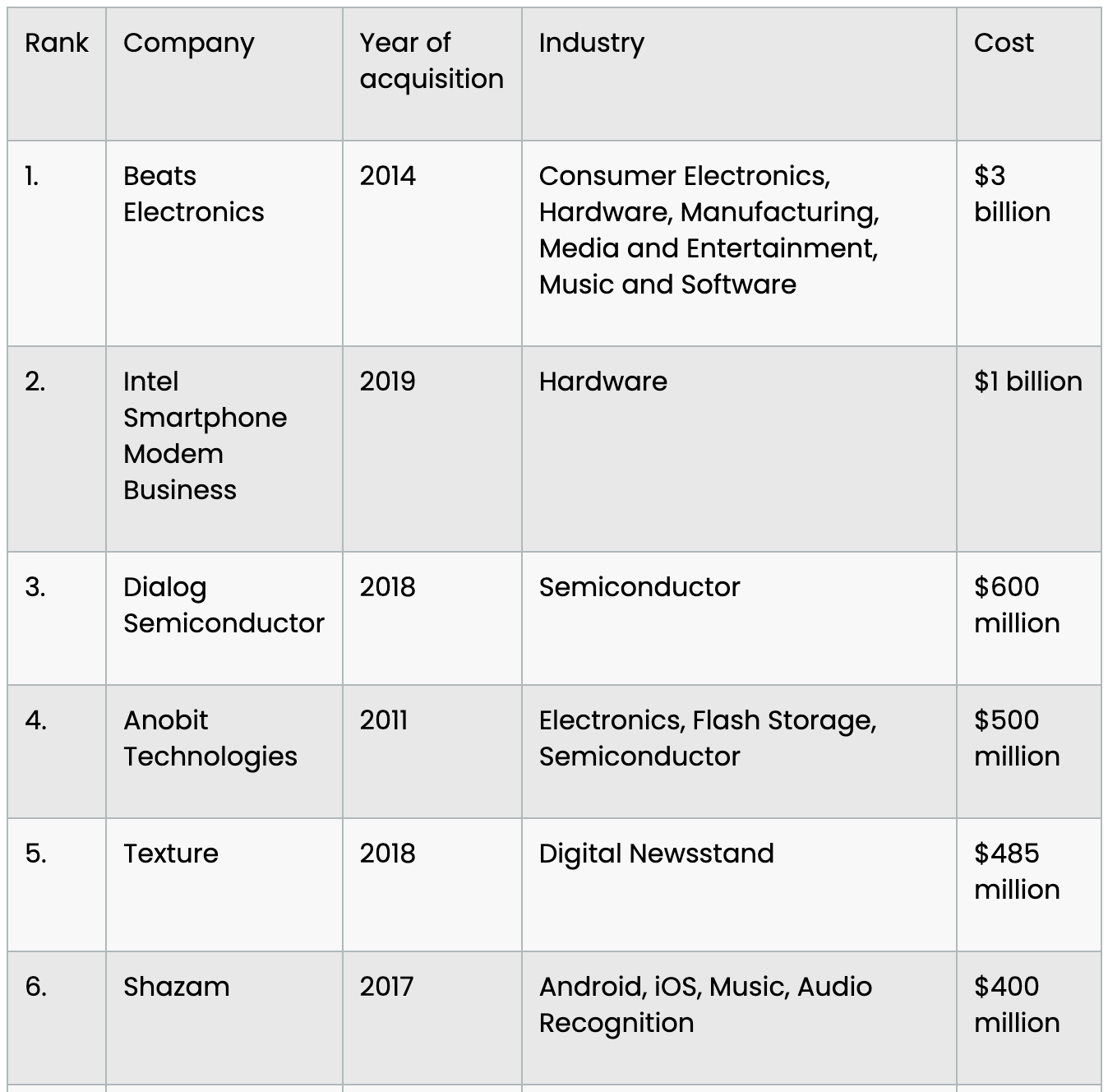

Apart from having huge adoption numbers, Apple has also made multiple strategic acquisitions over the years, with the most recent one being the acquisition of music label BIS Records, with future implementations in Apple Music. Other noteworthy acquisitions include Beats Electronics, Shazam, and Intel’s smartphone modem business.

Apple’s Top 6 Acquisitions By Valuation (forex.com)

The size and frequency of Apple’s acquisitions are a good reflection of the company’s business strategy, and strong levels of free cash flow. Apple actively acquires smaller companies, utilizing their technology to enhance its current products. An example of this is the acquisition of AuthenTec in 2012, giving rise to Apple’s first offerings of the Touch ID feature.

Future projects

Apple has announced numerous projects to be materialized in the coming years. Here are examples of a few.

Project Titan

In 2016, Apple reported to have embarked on a new initiative known as Project Titan – a program with aims to develop Apple’s very first electric car. The project itself saw a bit of a standstill in the first few years, especially in 2019 where over 200 employees working for the program were laid off as the company shifted its focus back to its original product developments. However, the project is still in the works today, and a Reuters report in 2020 revealed that Apple is still on track to create its very own electric car, and is also in the process of developing its own unique battery technology which

“bulks up the individual cells in the battery and frees up space inside the battery pack by eliminating pouches and modules that hold battery materials.” This battery design would allow for more active material to be packed inside, potentially offering longer range.”

Successful implementation of Project Titan could open doors to a completely new industry for Apple, and the growth this brings to the company fundamentally and financially cannot be understated.

Quartz

In 2023, a report on Bloomberg revealed Apple’s plans to launch Quartz – a digital health coaching service fully equipped with a multitude of physical and mental wellness features powered by artificial intelligence. The service itself is

designed to keep users motivated to exercise, improve eating habits and help them sleep better, according to people with knowledge of the project. The idea is to use AI and data from an Apple Watch to make suggestions and create coaching programs tailored to specific users.”

Quartz is set for its first release in 2024, though this is subject to changes. With successful implementation of Quartz, we see Apple taking several steps in the direction of healthcare innovation. Seeing how Apple Health has evolved over the years, an AI-powered wellness service could possibly bring even greater value to current Apple users, further strengthening the rate of adoption of Apple’s products.

Apple Vision Pro

Following the advancements in mixed reality technology, Apple has announced the imminent release of the Apple Vision Pro. Reports state that Apple Vision Pro is a

mixed reality headset is outfitted with displays that have a 90Hz refresh rate.”

Part of the new headset’s offerings include a virtual floating keyboard, and other mixed reality navigation features which can be controlled via our eyes, hands and voice. In the world of spatial computing, the Apple Vision Pro could be a technological breakthrough. The company is confident of releasing the finalized product early next year.

Financials

The reason why Apple is able to achieve the above feats is largely due to its strong financial position.

Free cash flow

As of 2022, Apple has $111.44b in free cash flow. This is a huge amount – just to put this into perspective, Apple’s free cash flow is worth more than the entire market capitalization of PayPal and Spotify combined. With strong levels of cash flow every year, Apple has been paying dividends to investors, buying back shares and engaging in strategic acquisitions – all of which are sound business decisions that benefit both the company and its investors.

Revenue growth

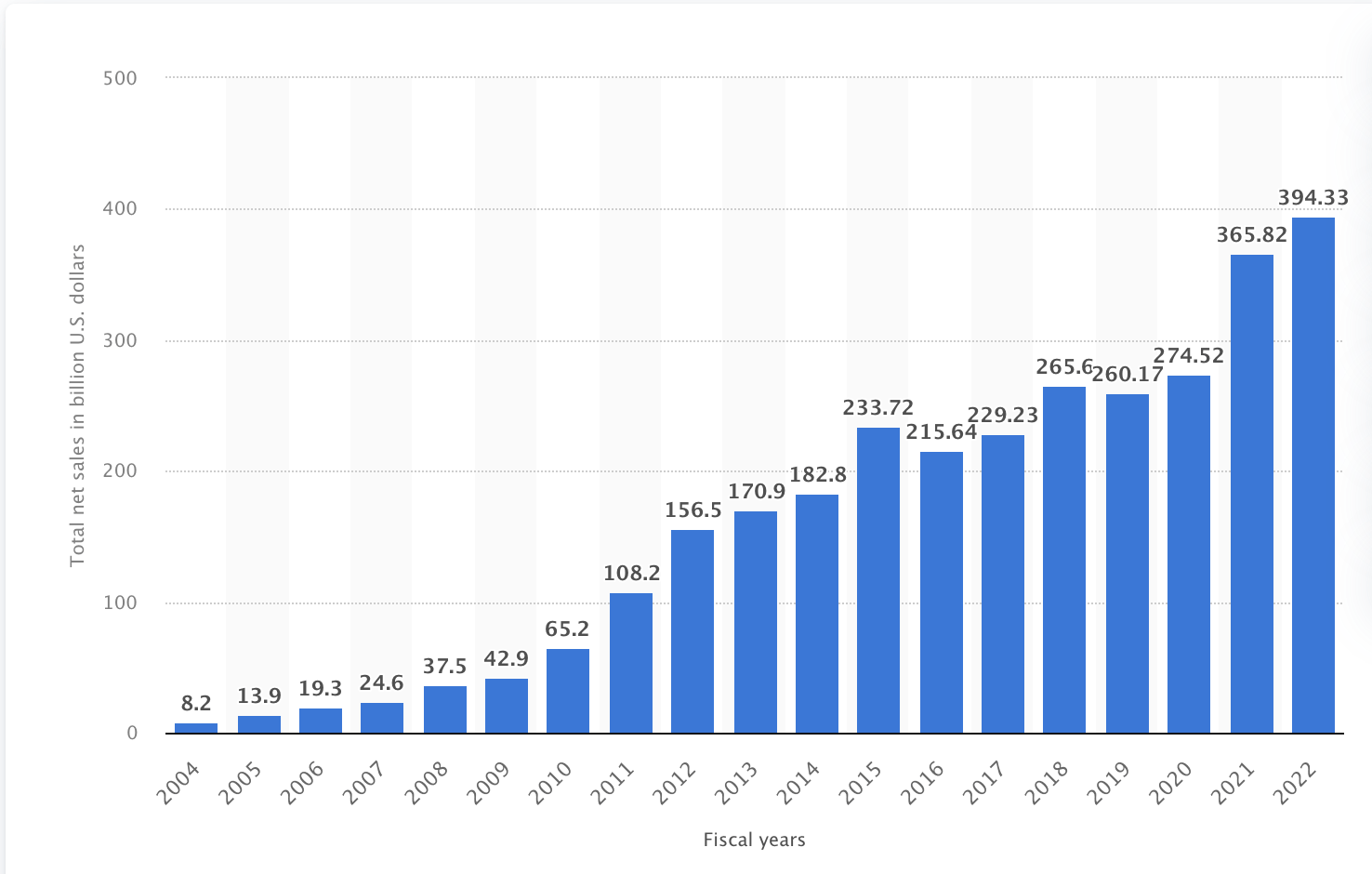

Apple’s revenue from 2004 to 2022 (Statista)

Apple’s immense revenue growth over the years cannot be understated. Through the development and sales of its various products, the company has managed to go from $8.2b in revenue in 2004 to a massive $394.33b in 2022, becoming the largest tech company in the world by revenue.

Gross Profit Margin

In 2022, Apple saw a gross profit margin of 43.31% – a great indicator of profitability. While Apple earns massive amounts of revenue, its decently high margins also indicate that they’re able to control their costs efficiently, hence bringing the company its strong cash flow position today.

Long-term debt to free cash flow (LTD-FCF) and long-term debt to EBITDA (LTD-EBITDA)

The LTD-FCF and LTD-EBITDA metrics are often used to evaluate if a company is financially able to fulfil its long-term debt obligations through its free cash flows and earnings respectively. With a long-term debt of $109.71b in 2022, Apple’s LTD-FCF is 0.98, and LTD-EBITDA is 0.84. With both these metrics below 1, it indicates that Apple is financially able to pay off all its long-term debt if it desires to, and this is definitely a favorable position to be in.

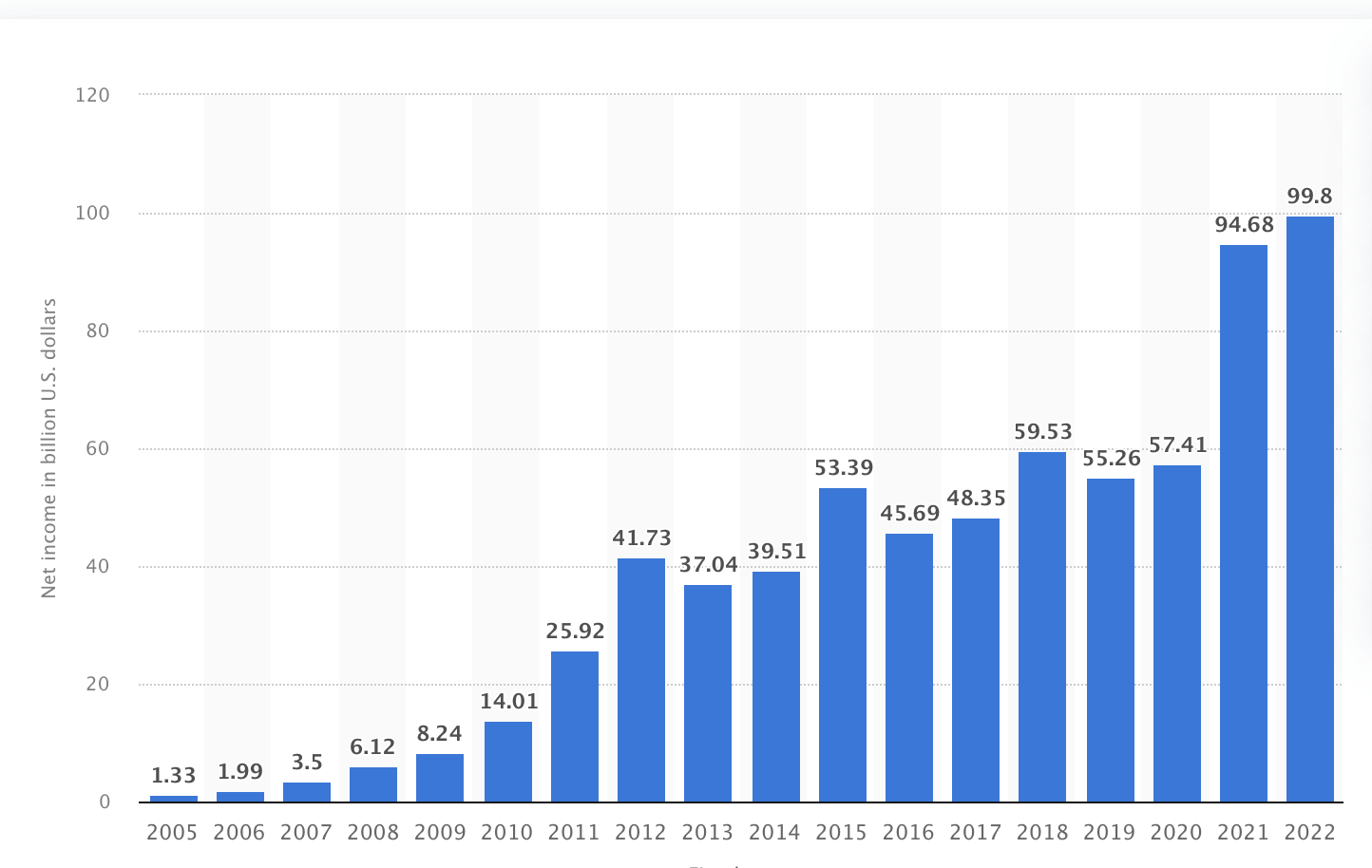

Net income

Apple’s net income from 2005 to 2022 (Statista)

We often use net income to evaluate a company’s bottom line – all things considered, is the company profitable or not? We see an exponential growth of Apple’s bottom line, from $1.33b in 2005 to $99.8b in 2022. Over the years, Apple has grown tremendously, and at the same time, as been increasingly profitable even after paying off its expenses. This is the hallmark of a good company.

The biggest concern

While Apple is a very strong company in the world of blue chips, there is one big concern that investors are worried about.

Apple’s growth is slowing. Will it continue to stay relevant and profitable?

While Apple has enjoyed exponential growth in many of its financial metrics over the past decade, its recent numbers could be signaling a slight fall off its original trajectory. According to analysts, Apple is set to finish the year with lower EPS and revenue compared to 2022. We see that iPhone sales are slowing down this year, and people are questioning if the company’s products can continue to remain relevant in the coming decade. After all, Apple has been the industry leader for so long now – could it potentially pass the baton to another company soon?

Personally, while this is a valid cause for concern, I am confident in Apple’s ability to innovate and adapt to current technological trends, but whether that is a certainty in the coming decade remains to be seen. One thing we need to remember is that Apple is no longer just a phone and computer producer. The company has developments in chip production, battery manufacturing, Metaverse products, electric vehicles and so many more areas. When factoring in the current financial strength of the company, along with the potential of its ongoing projects, I do believe that Apple can remain relevant and profitable.

Valuation

Now, we can all agree that Apple is a great company, but is it at a great valuation right now? We’ll be using a simple EPS projection to decide a fair valuation for Apple stock, but before we do that, let’s go over Apple’s recent financials.

Earnings per share (EPS)

Apple’s diluted EPS has grown at a compounded average growth rate of 19.7% YoY from 2018 to 2022, going from 2.98 in 2018 to 6.11 in 2022. A strong YoY EPS growth is a good indicator of profitability. However, due to Apple’s performance this year, analysts predict Apple’s diluted EPS in 2023 to be somewhere in the neighborhood of 6.07 – basically a drop of 0.65% from 2022.. This can be attributed to Apple’s slower financial growth at the start of this year. In Q1 2022, Apple reported a diluted EPS of $1.88, down 10% YoY. The subsequent quarters were slightly better, but analysts still maintain that the diluted EPS of year 2023 will be lower than last year’s figures.

Revenue

Apple’s revenue has grown from $265.81b in 2018 to $394.33b in 2022, representing a 10.4% compounded average growth rate. However, analysts predict that the company will finish the year with about $383.11b in sales. This is notably due to slowing revenue growth in 2023, having experienced its largest quarterly revenue drop YoY since 2016 in Q3 2023. This would mean a drop of 2.85% in revenue from 2022.

Shares outstanding

Apple has been buying back shares consistently, with its diluted shares outstanding decreasing from 20b to 16.33b, hence buying back a compounded average of about 5% of its shares every year. This is great for investors, whose stakes in the company get bigger and bigger as Apple continues to buy back shares with its free cash flow.

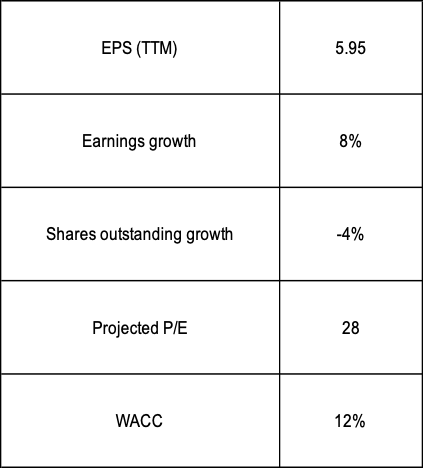

Assumptions

EPS Model Assumptions (Prepared by author)

Factoring in Apple’s recent financial situation, I have decided to use the above assumptions in my EPS projection model (over the next 5 years) to determine a fair valuation for Apple stock. I believe that 8% earnings growth and a 4% share buyback rate annually are reasonable estimates, after factoring in the company’s slowing growth numbers, and the potential additional cash invested into future projects.

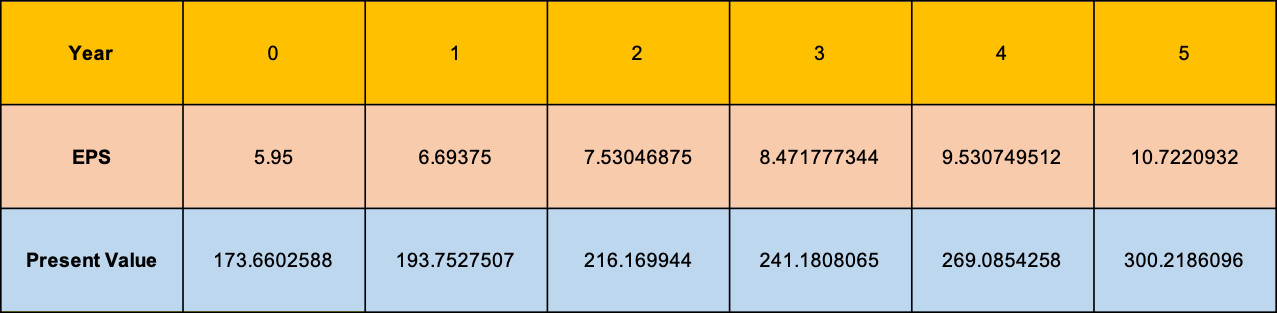

Fair value

EPS Projection (5 Years) (Prepared by author)

We see that we’ve come to a price target of $173.66, indicating that the current stock price of $171.21 is a potential bargain.

Experts’ analysis

In September 2023, Goldman Sachs and BofA Securities initiated price targets of $216 and $208 respectively for Apple, both higher than my final intrinsic valuation.

Investment decision

Apple Inc. is a company with strong fundamentals, and it continues to innovate during times of evolving technology and intense industry competition. Given its current valuation, I believe that investing in Apple is a sound investment decision. The current market price is slightly below my intrinsic value, and significantly below BofA and Goldman’s price targets. As such, I have issued a rating of “Buy” at a price target of $173.66.