Gustavo Muñoz Soriano

My last Apple (NASDAQ:AAPL) article in the spring here was a Sell rating, largely based on its extended valuation on “slowing” growth, with operating yields vs. rising interest rates making little sense. Well, the stock quote has risen slightly (+9%) over the last six months, analyst sales and EPS forecasts continue to weaken, AND interest rates in America are ever rising during 2023.

The logical conclusion is Apple’s overvaluation vs. reality may still be expanding. What does this mean for shareholders? Essentially, the odds of a steep price dive soon are accelerating.

Stagnating Growth

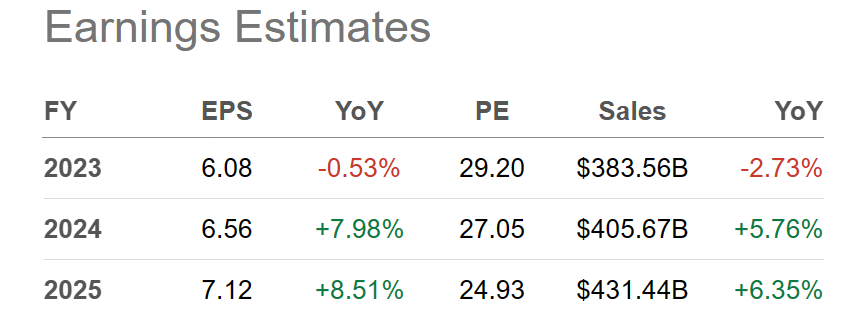

Earnings and sales growth has all but stalled in 2023 vs. 2022, while future gains are expected to be muted during 2024-25. Below is a table of growth averaging only +5% to +8% annually from the various metrics after this year, which isn’t far above the current CPI inflation rate of 4%.

Seeking Alpha Table – Apple, Analyst Estimates for 2023-25, Made October 6th, 2023

{kind=link}

More worrisome is the trend of analyst changes. Downward revisions over the latest 12 months looking at 2023-25 results is the new normal. This idea is graphed below.

YCharts – Apple, Analyst EPS Estimates for 2023-25, Made October 7th, 2023

Revenue growth is looking particularly weak. Reviewing actual performance stats, the last three quarters reported lower sales than the same period a year earlier. Below I have drawn the YoY quarter performance for revenue growth back to 1999. You will notice when we adjust for macro changes in inflation for the whole economy, the backpedaling is even more severe, around -5% this year. You have to go back to several quarters in 2016 and the 2001-02 technology bust to find similarly weak numbers.

YCharts – Apple, Quarterly Revenue Growth vs. Year Ago Period, Adjusted for CPI Inflation, Since 1999

Plus, Wall Street analysts have dramatically lowered sales projections for 2023-25, graphed below. If you are buying Apple for its strong future growth, I suggest you think through the math a little harder.

YCharts – Apple, Analyst Revenue Estimates for 2023-25, Made October 7th, 2023

My point is Apple is no longer a high-growth machine. In fact, net earnings and sales growth has become quite “subpar” in the Big Tech sector this year. If further issues develop for top and bottom-line numbers, it makes absolutely no rational sense to put above-average growth-based valuation multiplies on the company’s shares.

Overvaluation Story – Halloween Scary Now

However, Apple is now sitting at perhaps its richest valuation since at least 2006, if not the early 2000 tech bubble peak. Let me explain why.

Simple Fundamental Analysis

Believe it or not, Apples’ valuation on basic underlying fundamentals is DOUBLE the level of 10 years ago. Price to trailing earnings (29x), sales (7x), cash flow (25x), and book value (46x) seem to be anticipating well-above average growth from Apple. If investors were weighing the facts accurately, and understood the company’s quickly fading outlook, valuations should be closer to 10-year lows, not right underneath its 2021 Tech Bubble 2.0 peak.

YCharts – Apple, Price to Basic Fundamental Valuations, 10 Years

Again, when we include debt and cash levels, enterprise valuations on core cash EBITDA and overall sales are closer to 3x the ratios of a decade ago. This valuation is a little hard to fathom, if you believe in the efficient market theory. Unless a huge growth spurt is right around the corner, Apple’s valuation is a distance away from any easy to explain level in my opinion.

YCharts – Apple, Enterprise Valuations, 10 Years

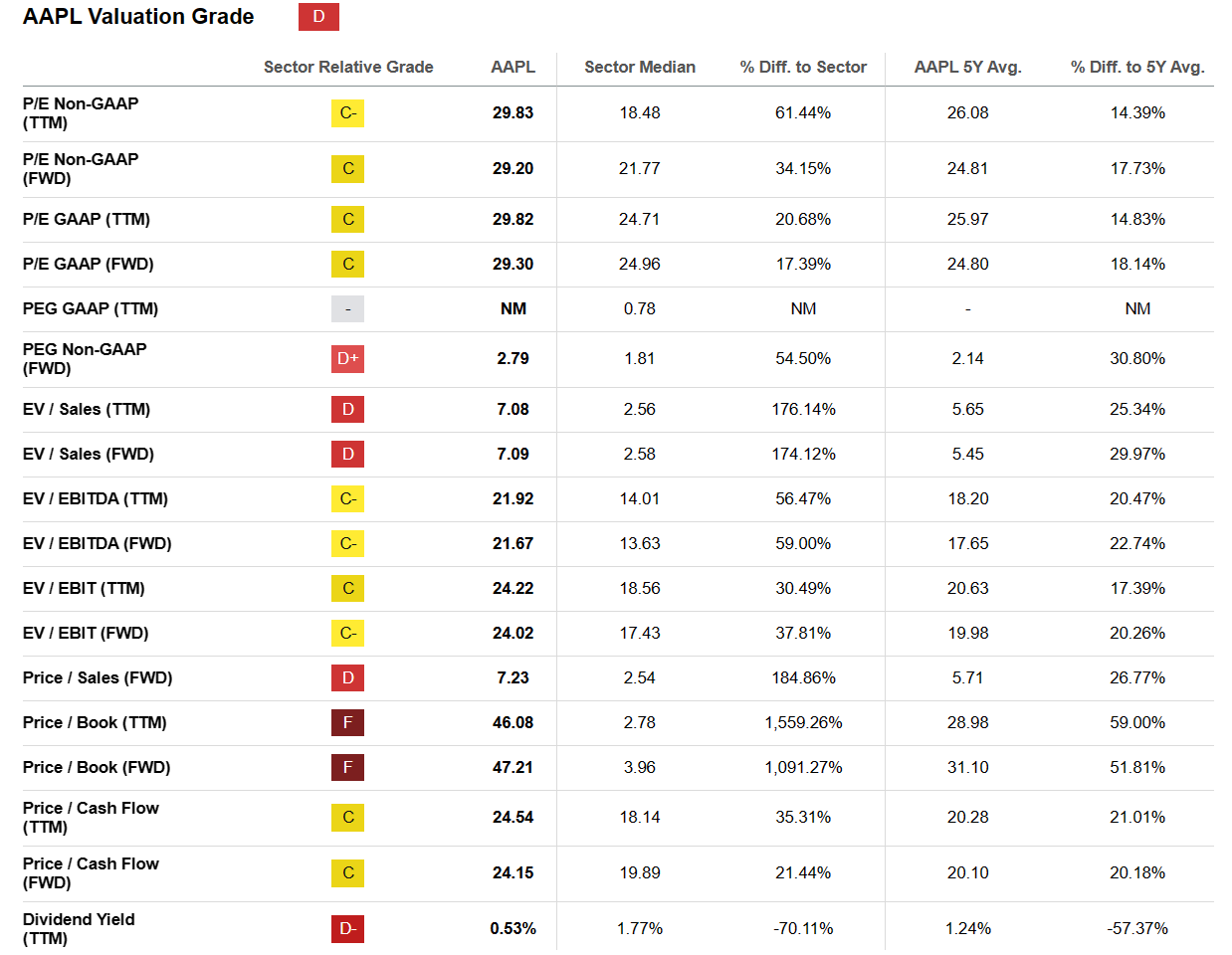

Seeking Alpha Quant puts a Valuation Grade of “D” on Apple. To me this is quite generous, especially when we turn our attention to rising interest rates as direct competition for investment capital and a source of textbook business valuations.

Seeking Alpha – Apple, Valuation Grade, October 7th, 2023

{kind=link}

Relative to Interest Rates

The truly bad news for Apple shareholders is the current extended valuation on basic fundamentals also makes no sense when compared to rising U.S. interest rates. When you invest in a business, one of the minimum bars to surpass for a return on your capital is the inflation rate. Another valuation yardstick is you want to earn more than Treasury security yields. Prevailing interest rates for bonds and bills issued by the U.S. government are considered the base “risk-free” returns to compare with all other investments. If an investor is guaranteed the return of their upfront capital, plus a specific fixed interest rate, riskier business ownership must beat Treasury returns.

Yet, Apple is failing to meet this minimum risk-free investment return idea in 2023, after generating a positive adjusted rates since 2008. Below I have charted the free cash flow yield (Warren Buffett’s preferred gauge which is often similar to the earnings yield calculation) relative to the 30-year Treasury bond rate, on 10-year and 24-year graphs. You will notice, Apple almost always has delivered an upfront free cash flow yield far better than 30-year government bonds since 2008.

YCharts – Apple, Trailing Free Cash Flow Yield vs. 30-Year T-Bond Rates, Since 2013 YCharts – Apple, Trailing Free Cash Flow Yield vs. 30-Year T-Bond Rates, Since 1999

Again, when we compare immediate free cash flow yield numbers to cash-like 3-month Treasury bills, new Apple investors have usually been able to buy a business delivering substantial value well beyond cash yields (at least between 2008-21).

YCharts – Apple, Trailing Free Cash Flow Yield vs. 3-Month T-Bill Rates, Since 1999

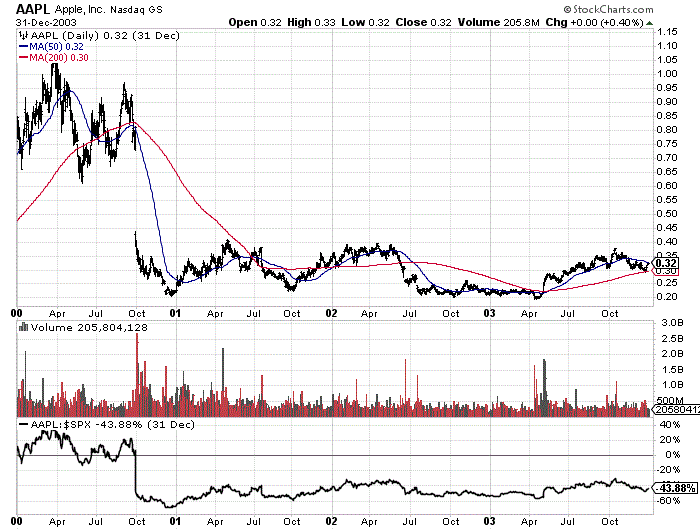

So, here’s where I think my analysis gets interesting. The last time both slow revenue growth and a large negative free cash flow yield adjusted to risk-free Treasury yields existed together for Apple was the original Dotcom Tech Bust of 2000-03!

Below is the Apple price and volume chart from January 1st, 2000 to December 31st, 2003. For me, this period is the most analogous to where Apple stands today, especially if a global recession and/or geopolitical trouble for the company’s China-dependent supply chain is next during 2024. Had you purchased Apple shares in the first half of 2000, losses of -75% or greater and relative losses vs. the S&P 500 index beyond -40% were the rule for years.

StockCharts.com – Apple, Daily Price & Volume Changes, Split/Dividend Adjusted, 2000-03

{kind=link}

Technical Trading Momentum

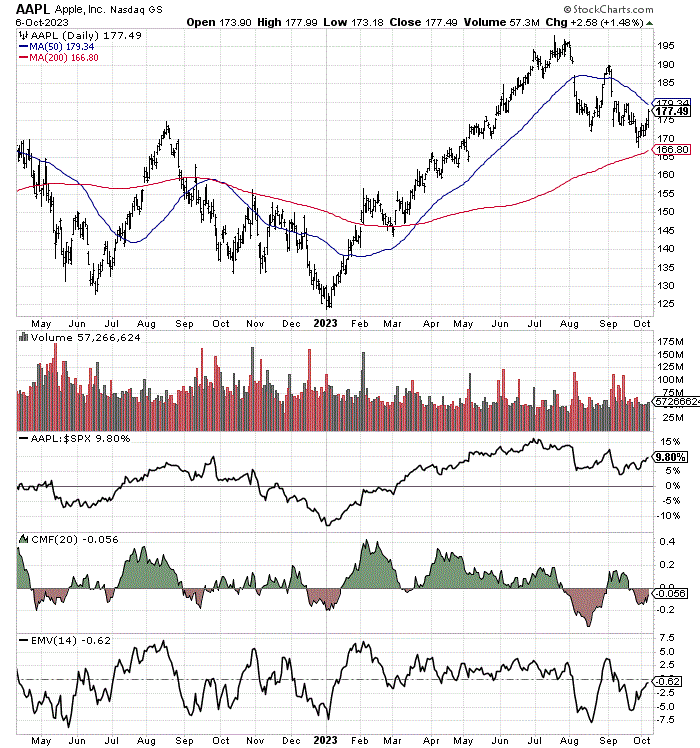

In terms of the technical trading chart today, Apple’s price weakness since July has included an unusual lack of transaction volume. On the 18-month chart below of daily price and volume swings, you will notice the late summer drawdown in price was a very low volume affair vs. the selling in 2022.

The 20-day Chaikin Money Flow and 14-day Ease of Movement calculations from August may be telegraphing the idea that few large-volume buyers exist at the present time. So, if new reasons to sell Apple appear, an absence of buyers to support price could be a problem in the immediate future.

StockCharts.com – Apple, 18 Months of Daily Price & Volume Changes

{kind=link}

Final Thoughts

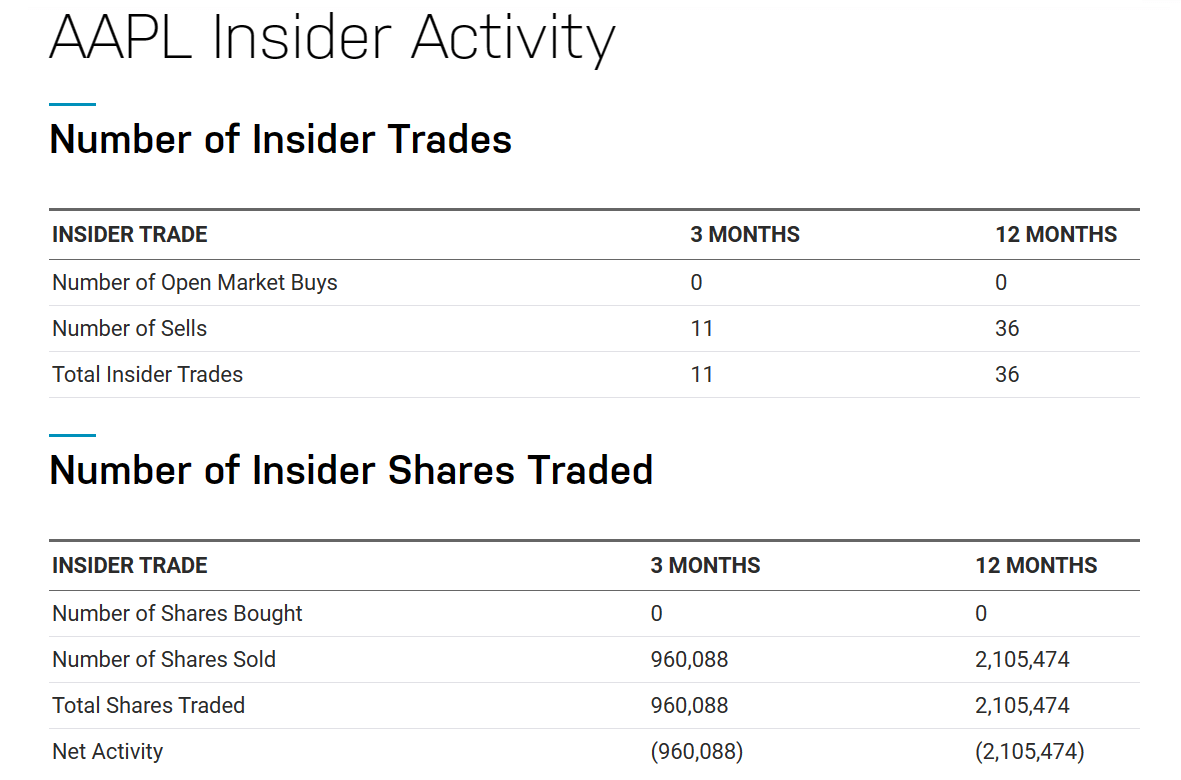

Insider sales are also becoming a worry. Apple’s CEO Tim Cook and an extensive group of top management just sold off tens of millions in stock value. In addition, there have been ZERO insider buys reported by directors and management over the latest 12 months. I believe the readout is insiders running the business do not think shares are either inexpensive today or growth will be stellar next year. Below is a table summary of SEC insider transaction reports taken from the Nasdaq website, including roughly $300 million in net liquidations.

Nasdaq.com – Apple, Insider Trades, 12 Months

{kind=link}

Outlier supply-chain risk out of China is another big-picture concern. The Chinese government appears to be cracking down on Apple product demand, in retaliation for U.S. prohibition on technology industry sales to this important country. In early September, the Chinese government mandated workers stop using Apple iPhones (and foreign-branded smart phones). Hurting a major demand market for the company (China/Taiwan accounted for 19% of 2022 sales), Apple shares slid -8% in kind. On top of this issue, Apple’s whole supply chain for computers and gadgets is centered on cheap Chinese/Taiwanese production, with the help of contractor Foxconn. So, this U.S. business is particularly susceptible to any potential China vs. Taiwan military war.

In all honesty, Apple’s overvaluation today may be directly linked to Warren Buffett’s large ownership stake through Berkshire Hathaway (BRK.A) (BRK.B). Without Berkshire’s 7% position in the company, and related confidence created by its holdings, a far lower share quote would already be today’s reality.

For my money, I am considering buying Coca-Cola (KO), another major Berkshire holding. It sports a similar net profit margin of 24% to Apple’s 25%, has a growth outlook into 2025 that looks identical (annually EPS +7%, sales +5%), is less dependent on China for its operational success, should survive a global recession better, and is delivering a stronger cash dividend yield of 3.5% right now vs. 0.5% from Apple. In the end, all of these relative positives for KO are available at a valuation making more sense for investors, especially considering its “defensive” consumer beverage focus. I would rather own Coca-Cola’s equally positive investment setup at a P/E of 20x for example, than Apple’s valuation on earnings closer to 30x.

When I pull all the ideas together, I come up with a fair value for Apple closer to $125 per share presently. In my view, a forward P/E level of 20x from this traditionally “cyclical” business would properly account for China supply chain and worldwide recession risks. You have to remember, if we do get an economic downturn in 2024, Apple’s sales and earnings will likely DECLINE markedly vs. current analyst forecasts. And, with risk-free savings and Treasury bond rates around 5%, cash alternatives maintain sound logic to own over the coming 12 months. In a deep recession, falling Apple EPS and free cash flow may only support a price of $100 sometime next year.

What environment could hold up the share price? The bullish argument to keep Apple trading in the $150 to $200 range in 2024 is essentially a “goldilocks” outcome for the economy. If global inflation declines back to 2%, while the economy picks up steam into the 3% range for real GDP growth, at the same time as U.S./China relations improve dramatically, Apple might be able to beat current operating expectations.

For sure, a lower interest-rate backdrop may now be necessary to support the Apple quote and valuation above $150. If global interest rates keep rising into early 2024, Apple will find it incredibly difficult to stay near $175 for price.

I reiterate my Sell rating. At prices around $200 per share, I would move my rating to Strong Sell, all other variables remaining the same.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.