Keith_Rose

After the bell on Thursday, August 1st, we’ll get fiscal third quarter results for the June ending period for Apple (NASDAQ:AAPL). The technology giant is one of the companies I have covered the most on this site over the last decade, but I’m heavily leaning towards not covering this quarterly report. The main reason is that the recent surge in Apple shares has essentially made these to be reported numbers irrelevant in my opinion. The more important parts of the story will play out later this year, as Apple looks to make a major push into artificial intelligence (“AI”) with its next line of iPhones.

A quick look back:

When I last covered the name, the stock had seen a relief rally after fiscal Q2 results were not as bad as some were expecting. While the company did report top and bottom line beats, expectations had come down quite significantly. In the end, a 4.3% revenue drop and penny per share earnings increase were detailed, along with another dividend and buyback hike.

Apple shares had not taken part in a lot of the AI rally earlier this year, as concerns over slowing iPhone growth limited share upside. I have kept a hold rating on the stock over time, as my long term bullishness for the company has been offset by some valuation concerns. Since my last article, Apple shares have rallied more than 24% to new highs, playing a little catch up to some of its peers, while the S&P 500 has managed a gain of more than 7%.

This year’s iPhone launch:

I’m sure street analysts will have lots to say as usual about the June quarter report, but I’m not exactly waiting for the numbers. To me, it doesn’t really matter if iPhone revenues are a billion better or worse than expectations, for example, as almost everyone is more interested in this year’s smartphone launch. In fact, expectations seem rather low given Huawei’s rebound and some other factors, which could be hurting iPhone sales in both China and the US (see here and here). In fact, one might actually make the argument that weaker iPhone sales now are better, as it could suggest consumers are waiting for the next phone to come.

Apple previewed some of its newest software at June’s developer’s conference. iOS 18 is built around the company’s new AI feature set, with a complete overhaul of Siri. A number of analysts believe that Apple’s major push into AI this year will spark a massive upgrade cycle for the iPhone, leading to the next significant leg higher in the company’s revenue growth story.

Like previous launches, Apple will unveil its latest iPhone chipset and upgrade its camera setup with this year’s four smartphones. It’s not certain yet if the company will provide a better chip with the Pro versions to separate them, but that’s again a possibility. One of the biggest changes expected is that the Pro models will get bigger, meaning the rumored 6.9 inch display on the Pro Max will be even closer to tablet size.

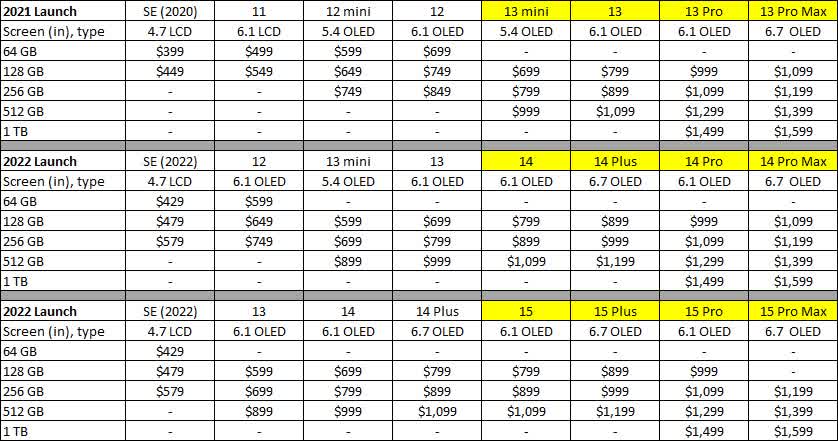

Perhaps the biggest non-AI headline surrounding launch day could be around pricing. Between the increase in size of the Pro models, as well as all of the AI stuff, it would not surprise me if we see some price hikes. With Apple and other phone makers trying to make these devices a bigger part of our lives, asking for a little more for them isn’t necessarily crazy. An extra $100 here may seem extreme, but over a two year plan you’re only talking about $4 or so a month. If these phones are as great as some expect them to be, you can also expect the carrier wars to be quite fierce. The graphic below shows the iPhone lineup the last three years, with the year’s main line launch being those highlighted in yellow.

Yearly iPhone Lineup (Apple Website)

{kind=link}

The switch from the Mini to Plus helped pricing a little, as did increasing the storage tiers of some models. Going to 1 TB versions on the non-Pro models could certainly help average selling prices as well. It’s even possible that this year’s phones all start with 256 GB of storage as part of a potential price hike. Apple doesn’t report unit sales for its products anymore, but even holding them flat could still mean an increase in total iPhone revenue if we do get higher overall pricing this year.

Is valuation now a problem?

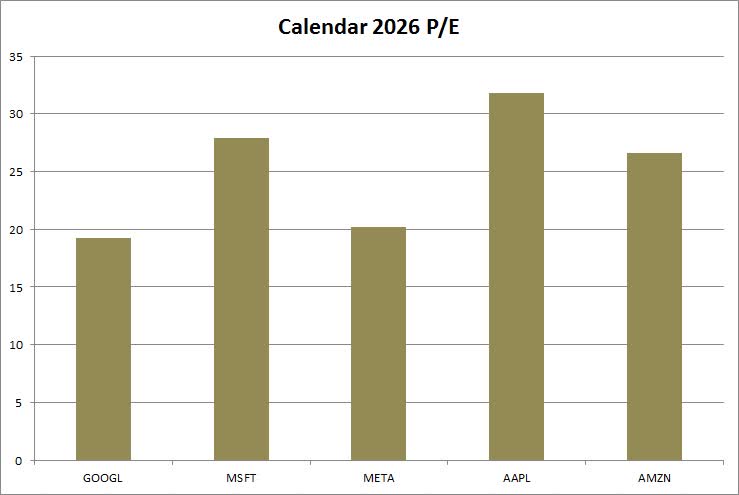

While Apple shares are up more than 16.5% in the past month, future earnings per share estimates aren’t moving that much at all yet. As a result, Apple’s valuation has been pushed up quite a bit when looking forward to calendar 2026. The chart below shows Apple against its large cap tech peers – Microsoft Corporation (MSFT), Alphabet Inc. (GOOG) (GOOGL), Amazon (AMZN), and Meta Platforms, Inc. (META). These price to earnings numbers are based on current analyst expectations for each in the twelve months of calendar 2026, regardless of what fiscal period that is for each.

Calendar 2026 P/E (Seeking Alpha)

{kind=link}

At almost 32 times, Apple is almost four points higher than the next closest name on the list, Microsoft. In fact, Apple’s P/E here is about 35% higher than the average of the other four, and it doesn’t exactly have the best growth profile of the bunch. I’ve talked in the past about buying Apple in the low to mid 20s when looking at the following year’s earnings per share, but Apple is in the low 30s right now and that’s an extra year out plus some.

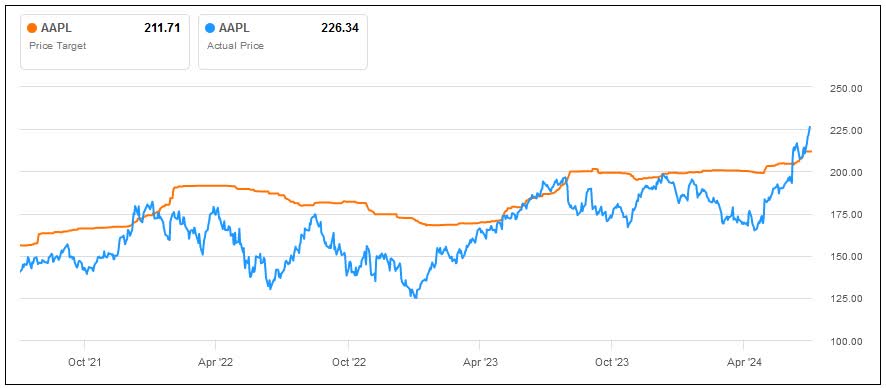

The recent rally in Apple shares has been so sharp that the stock is now nearly $15 above the average price target on the street. Despite numerous target hikes over the past month, the analyst average currently implies about 7% downside from here. While past performance isn’t always an indication of future results, the chart below shows that the time when shares are above the street average is not a good one to buy if you’re looking at performance over the next couple of quarters.

Apple Shares vs. Average Price Target (Seeking Alpha)

{kind=link}

Final thoughts and recommendation:

With Apple shares taking off on artificial intelligence hopes surrounding this year’s iPhone launch, the fiscal Q3 earnings report may be the least important one we’ve seen from the company in some time. With analysts expecting a major upgrade supercycle to start with the iPhone 16 line, I don’t see how it matters how smartphone sales fared in the last couple of months. The iPhone is still the overall revenue leader for Apple, so how it fares generally will impact whether the headline numbers beat or miss expectations.

With the hopes that Apple’s next leg of growth are ahead of it, I’m going to maintain my hold rating on the stock today. While I’m not a big fan of the valuation here, I don’t want to bet against this name in the long run. While a pullback would certainly be nice for those looking to enter, sentiment looks to be improving as the next line of products gets closer to launch. Of course, with shares surging recently, sales expectations will certainly be high later this year. Apple will have to deliver or we’ll likely see a “buy the rumor, sell the news” kind of story here.