Justin Sullivan

AAPL – why we like it around $170

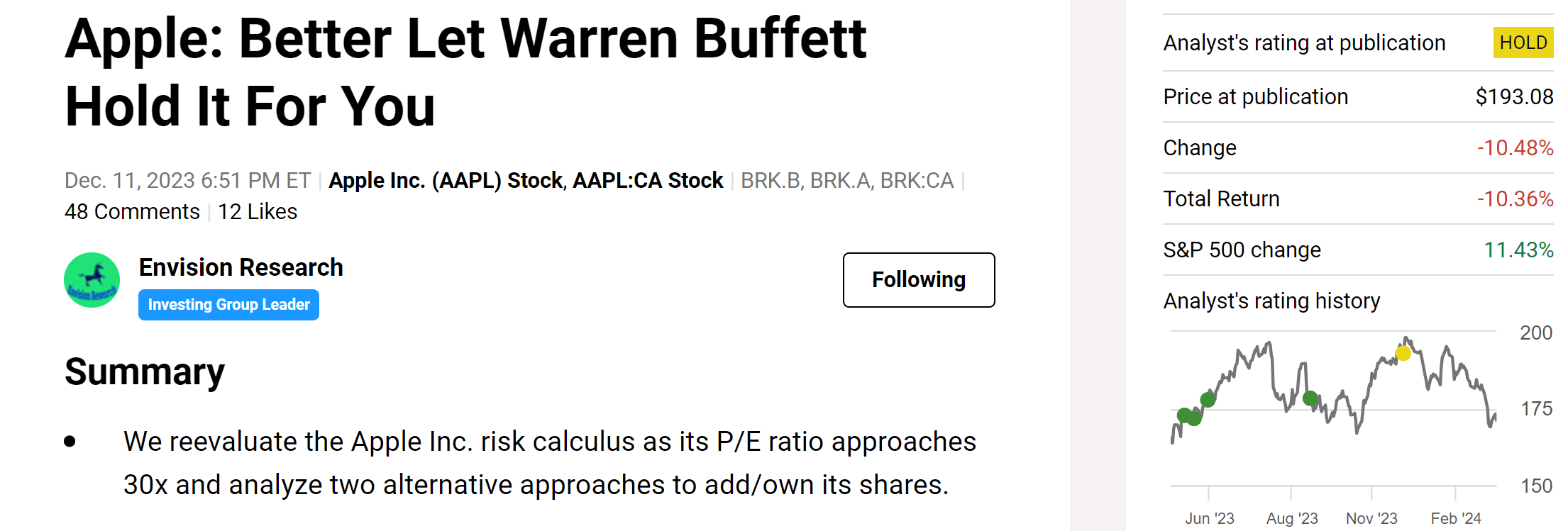

The goal of this article is to update our thesis on Apple Inc. (NASDAQ:AAPL) and upgrade it from HOLD to BUY. We last covered the stock back in Dec 2023 (see the figure below). In that article, we evaluated the investment risks as its prices hovered around a record high (around $193 as seen) and its P/E pushed to ~30x. The article then suggested two possible ideas at that time: 1) waiting till its price revisits the ~$170 level; and 2) holding AAPL shares indirectly via Berkshire Hathaway (BRK.B).

{kind=link}

Our previous article concentrated more on the second idea, detailing the crucial advantages of owning AAPL shares via BRK (such as “ownership P/E” and long-term compounding in a very tax-efficient way.

In this article, we will look into the first idea further, as the stock prices now have corrected to be close to the $170 level (~$172 as of this writing. I will argue why this price level is an attractive entry point for us. The remainder of this article will detail the key factors that went into our argument. These factors involve AAPL’s wide moat, some of its long-term growth, and its return potential relative to the broader market.

Why AAPL stock prices corrected?

As aforementioned, AAPL stock prices have suffered a sizable correction in the past few months, dropping by more than 10%. There are certainly some good reasons for such corrections. I will next scrutinize some of the possible reasons one by one and argue why these corrections are overdone, only reflect short-term market thinking, and have created a healthier entry point for long-term investors.

The first reason, which is the most logical to me, is that AAPL’s valuation is simply too high at a price level near $200 as argued in my earlier article. Apple’s stock had a significant run-up in 2023 and pushed the valuation to a bubbling regime, and a correction was potentially inevitable. The corrections, by bringing the P/E to a more normal level, are actually healthier for long-term investors (more on this in a later section).

The second possible reason is the potential slowdown in its China market. It is true that there have been declines in sales in China, a major market for many of Apple’s flagship products such as its iPhone. And there might also be other fundamental headwinds there, such as a shift in consumer preference there, competition from companies like Huawei, and also government restrictions on the use of AAPL products. However, my view is that these factors could eventually be short term (for example, if you share Warren Buffett’s investment timeframe). Moreover, even in the case that these headwinds become secular, I think there are plenty of other positive catalysts that could make up and continue driving growth in the long term, as elevated immediately below.

The growth of service revenues

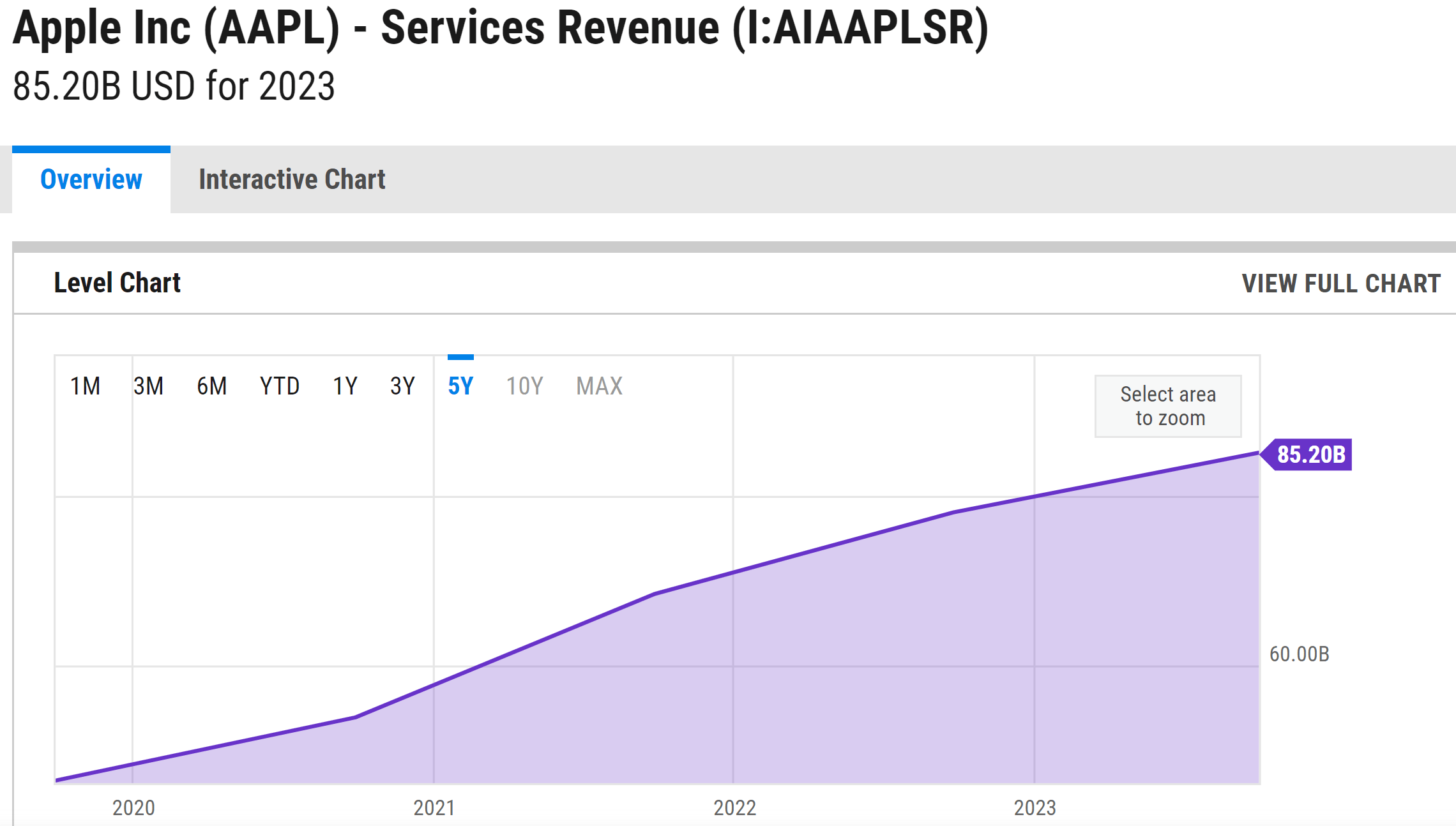

The top driver in my mind is the growth of service revenues in the long term. To be sure, I am optimistic about the company’s product lineup overall, ranging from the iPhone 15 lineup to the new MacBook Pro, and the Apple Watch Series 9 and Ultra 2. These products are hugely popular and continue to win over more fans (speaking from first-hand experience as the parents of a teenager and his friends). But what is more important to me, in terms of business fundamentals, is that the popularity of its hardware is translating into strong growth in its services segment (see the chart below).

I anticipate the growth in services revenues to continue and be a key return driver for several reasons. First, service revenues are stickier and enjoy higher margins than hardware sales. Second, AAPL’s service revenue growth is supported by a vast installed base. Apple’s installed base of active devices clocks in at over two billion, with well over one billion in paid subscriptions. These levels are almost double the tally from only about three years ago. Based on its last earnings report, services accounted for 25% of the top line in recent quarters, up from 20%~21% a year ago.

{kind=link}

APPL’s projected returns

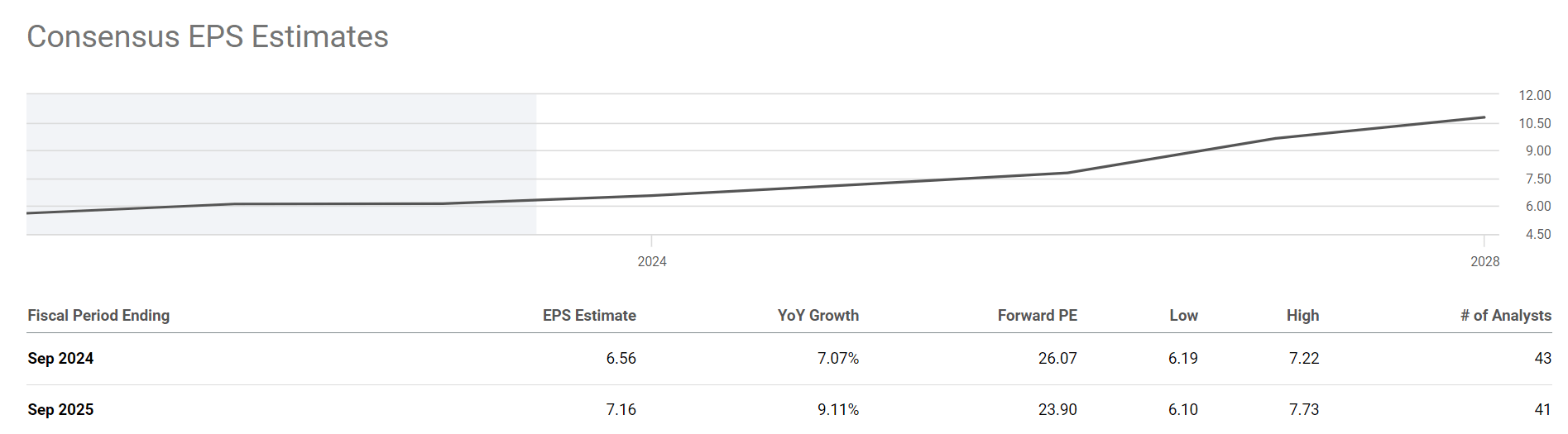

Now, let’s revisit an earlier point about the correction. I mentioned earlier that the corrections, by bringing the P/E to a more normal level (26x for FY1 and 24x for FY2 as seen in the charts below), are actually healthier for long-term investors.

{kind=link}

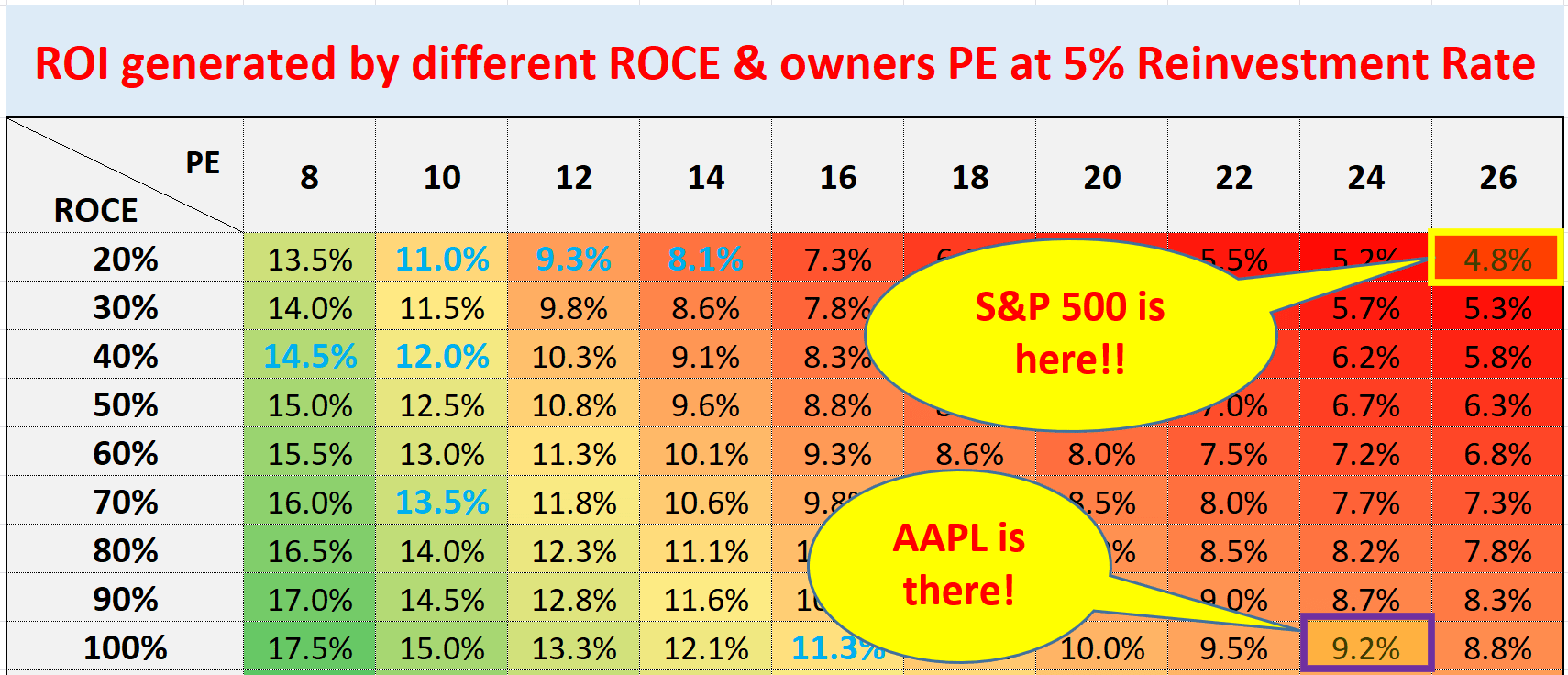

At these valuation levels, I project far better return potential from AAPL than the overall market. My projections only involve simple reasoning and napkin math, as detailed in the earlier article. The gist is that:

AAPL’s ROCE (return on capital employed) is nearly 100%. With such ROCE, a 5% investment rate would fuel 5% organic growth (100% ROCE * 5% reinvestment rate). As a result, any P/E near or below ~25x is attractive. A ~25x P/E provides ~4% of earnings yield. Considering AAPL’s capital-light model, the true owners’ earning yield must be higher than 4% (around 6% by my analysis). Thus, the total return in the long term is close to 10%, far better than the overall market’s penitential (projected to be around ~5% as seen in the chart below).

{kind=link}

Other risks and final thoughts

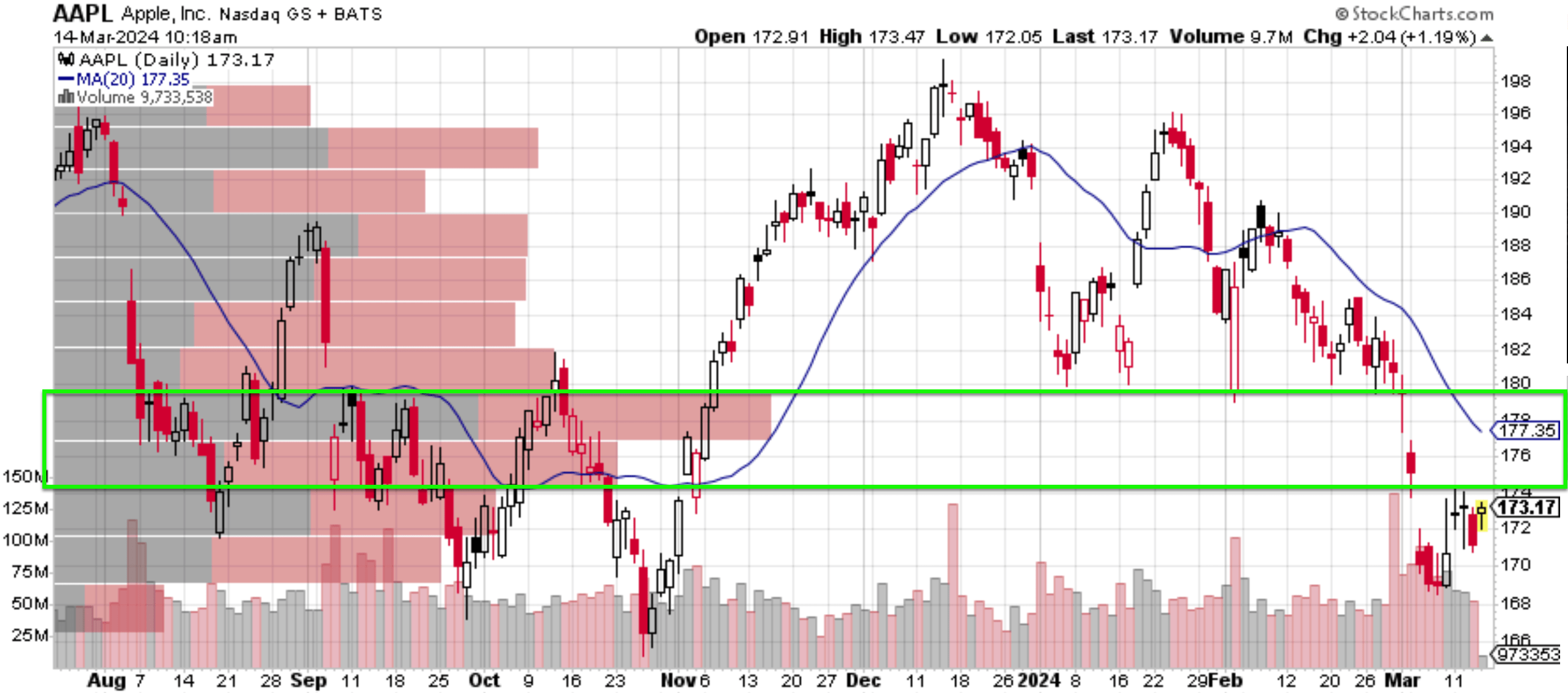

Before closing, a few risks are worth mentioning, both in the upward and downward directions. In the upward direction, the current price is close to a support level, as shown in the chart below. As seen, $175~$185 was the range where the heaviest trading volume has occurred in the past few months (as highlighted by the green box), providing support for further corrections below this level.

{kind=link}

In terms of downward risks, AAPL faces all the risks common to other technology stocks such as competition, technological obsolescence, global supply chain disruptions, et al. However, there are a few risks that are more particular to Apple’s business model. First, Apple relies heavily on a limited number of contract manufacturers, primarily in Asia. Disruptions at these factories could significantly impact production and lead to shortages. Second, it can be argued that AAPL has been a laggard on several technological fronts. These areas include the use of artificial intelligence and VR (virtual reality). The success of its Vision Pro headset is unclear and so far, it lacks a blockbuster AI products in my view.

All told, as a value-oriented investment focusing on the long-term, I think the Apple Inc. upsides outweigh the downsides under current conditions. There may be (will always be) speed bumps and corrections along the way. However, I think its core moat remains intact in the long term. As argued in the past, a large part of its moat is its premier brand and not only the technology. The rapid growth of its service segments only helps to further widen the moat. With this, let me close by repeating my final verdict. Owning shares of AAPL near ~25x P/E comes as a no-brainer for me in the long term. Even higher P/E ratios could be justified when held indirectly via BRK (of course, in this case, it depends on the valuation of BRK shares as detailed in our earlier analysis).