Ирина Мещерякова/iStock Editorial via Getty Images

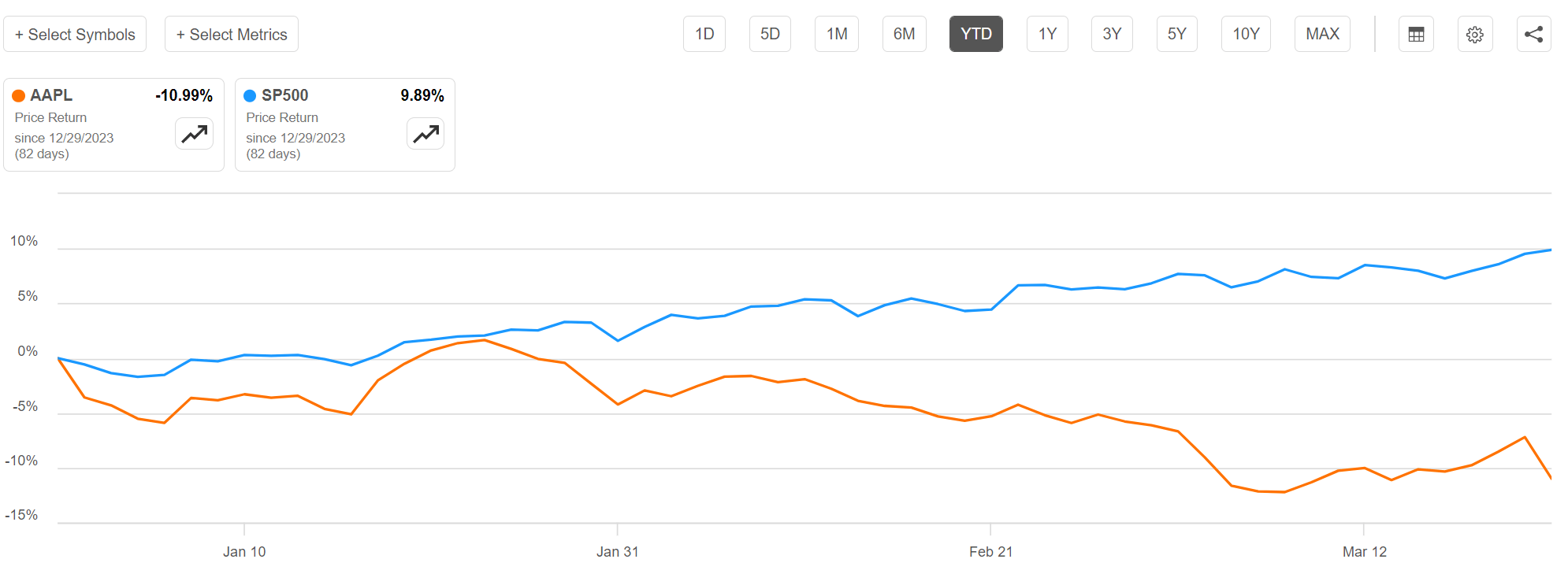

Recently, a bunch of negative catalysts have been pummeling the shares of Apple Inc. (NASDAQ:AAPL), with Apple shares declining by 11% YTD while the S&P 500 Index (SP500) has rallied by 10% (Figure 1).

Figure 1 – Apple has declined by 11% while the S&P 500 has rallied by 10% (Seeking Alpha)

{kind=link}

The most recent catalyst has been an antitrust lawsuit launched by the U.S. Department of Justice (“DOJ”) against Apple’s alleged anti-competitive practices.

Antitrust Lawsuit Is The Latest Blow To Apple

Antitrust concerns against Apple are not new. In fact, I wrote a cautious article on Apple’s European antitrust issues more than a year ago, when the European Union passed legislation (Digital Markets Act) to force Apple and other large digital gatekeepers to open up their platforms to competitor payment options.

In the latest case, the DOJ is alleging that Apple has been abusing its iPhone monopoly to prevent other companies from offering competitive services like digital wallets or cloud streaming services. The suit also alleges Apple limits the functionality of Apple’s hardware and makes it difficult for users to switch to and communicate with competitor devices.

As an Apple iPhone user myself, I am acutely aware of this difficulty, since I have longed desired to try out competitor phones like the Samsung Galaxy Z flip phone. However, because I have tens of thousands of family photos stored in my Apple Cloud account without an easy way to port my files to a competing cloud storage service, I am effectively “locked in” within the Apple ecosystem.

Unlike previous antitrust lawsuits and actions, the latest DOJ suit against Apple may be a little harder for investors and the company to brush off due to the high profile nature of the accuser. Simply put, even if the DOJ’s suit is meritless (and in my opinion, it certainly has merit), the DOJ, with its near limitless resources, can mire Apple in court for years to come.

Historical Precedent Signals Lost Decade

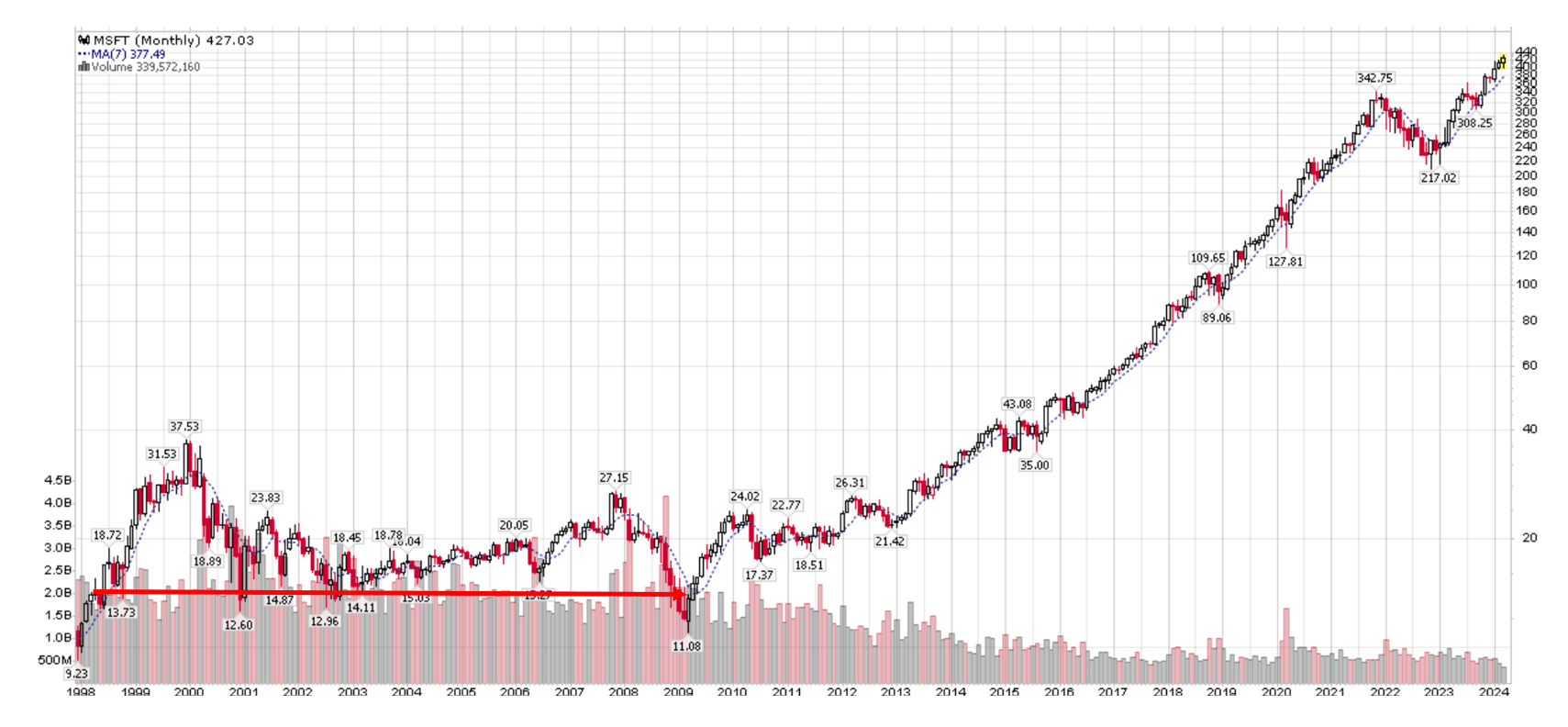

In fact, one interesting historical anti-trust precedent was the DOJ’s late 1990s lawsuit against Microsoft Corporation (MSFT), which heralded a lost decade for the company. Measured from when the government formally filed its lawsuit against Microsoft in May 1998, the company’s stock essentially went nowhere for more than a decade (Figure 2).

Figure 2 – Microsoft stock went nowhere for a decade after DOJ lawsuit (StockCharts.com)

{kind=link}

In the Microsoft case, although the DOJ ultimately won, Microsoft’s penalty was not terribly severe, as it settled with the government by allowing PC manufacturers to adopt non-Microsoft software.

However, arguably, the time and effort spent battling the lawsuit diverted key management attention and contributed to a “lost decade” for the technology giant, including missing out on search (Yahoo, then Google), music (iPods), social media (Facebook) and handsets (iPhones).

Stagnant Growth Is The Main Issue

Similarities between circa 2000 Microsoft and 2024 Apple goes beyond the current antitrust lawsuit from the DOJ. If readers can recall, back in 2000, Microsoft was the 800-lb gorilla in the technology space, with dominant positions in PC operating systems, web browsers, and productivity software. However, because of its dominant position, growth was also getting increasingly difficult for Microsoft, just like it is for Apple today.

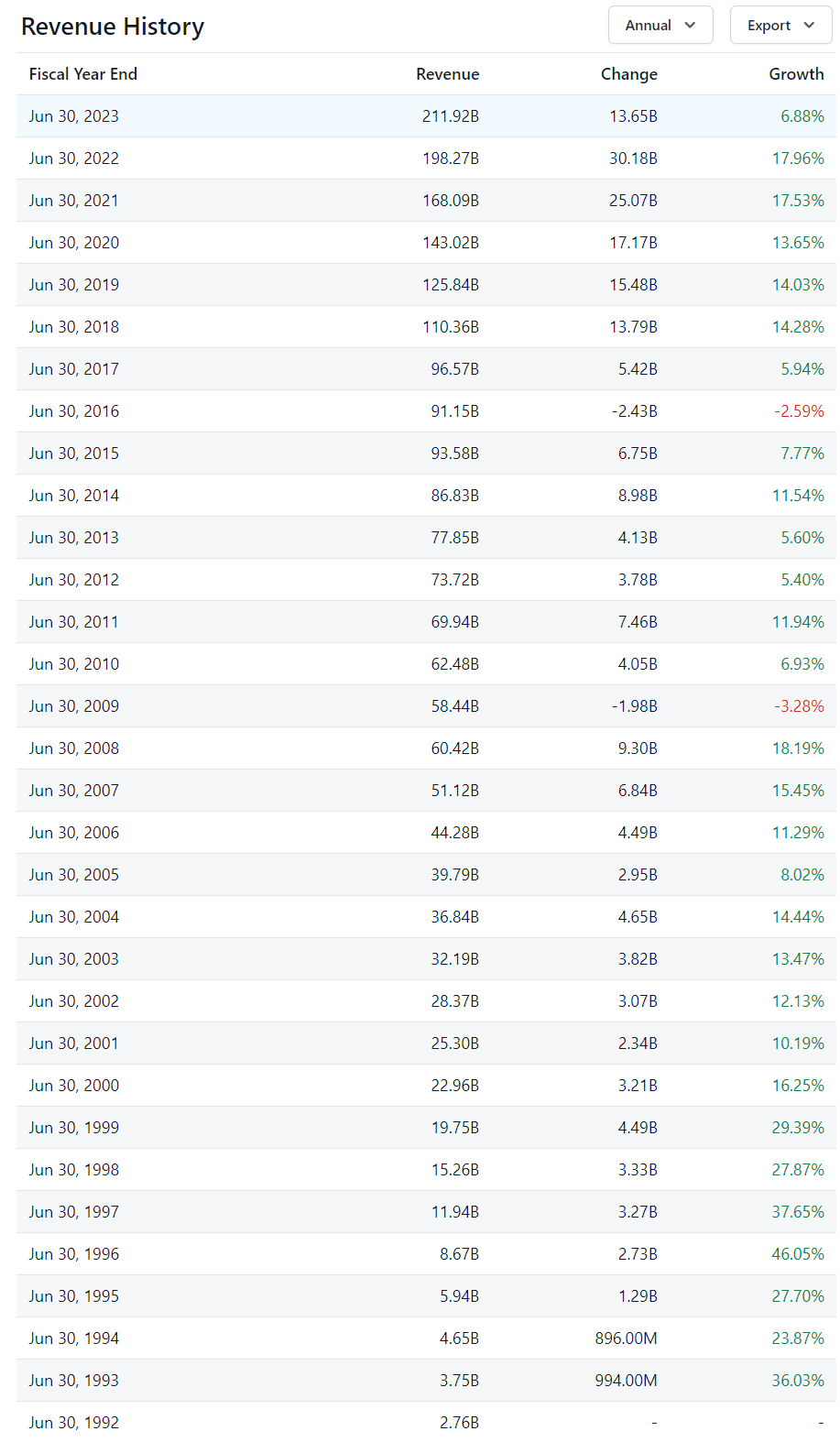

Microsoft’s top line revenue growth decelerated from ~30% in the late 1990s to ~10-15% in the early 2000s, causing the company’s valuation multiple to compress and its stock to stagnate (Figure 3).

Figure 3 – Microsoft annual revenues and growth rates (stockanalysis.com)

{kind=link}

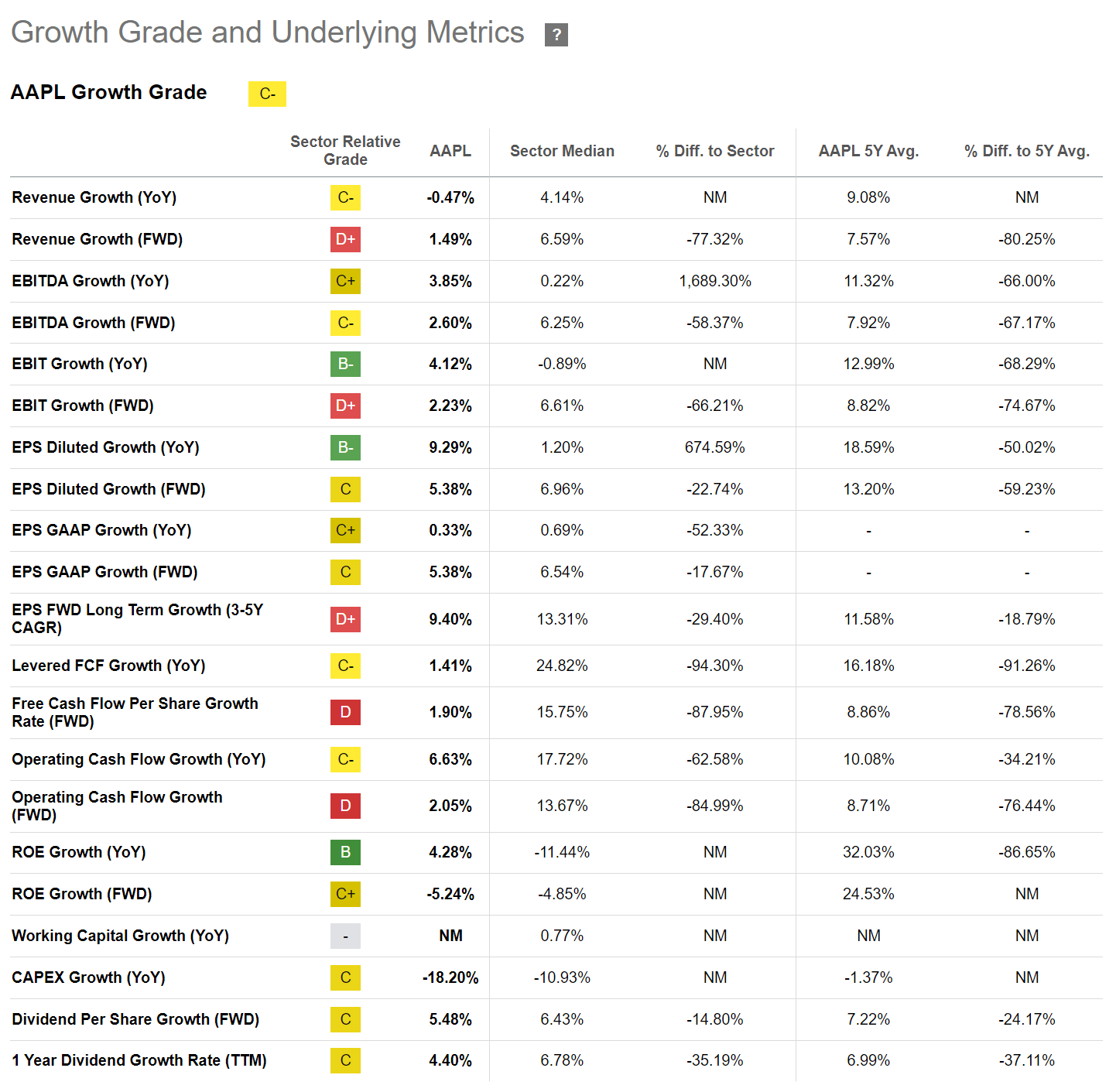

For Apple, the deceleration in growth is even more acute, as revenue growth has fallen into negative territory in the latest fiscal year (Figure 4).

Figure 4 – Apple growth has turned negative (Seeking Alpha)

{kind=link}

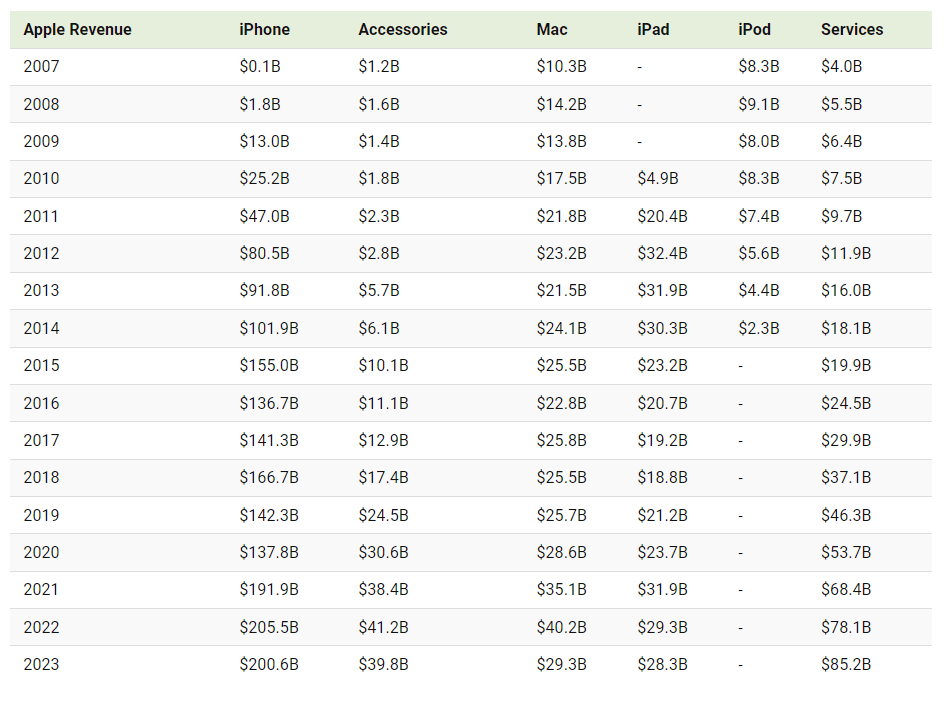

With a user base of over 1.5 billion, Apple has basically reached the saturation limit for its premium-priced products, with all business segments except services seeing declining sales in 2023 (Figure 5)

Figure 5 – Apple segmented growth (Visual Capitalist)

{kind=link}

Giving Up On The iCar…

For many years, Apple bulls were sanguine about the company reaching the physical limits of selling iPhones and iPads, as Apple had been rumored to be working on a fully autonomous vehicle (“Project Titan”) since 2015. With auto unit prices in the tens to hundreds of thousands of dollars, a successful vehicle launch could easily have ignited the next leg of growth for the trillion-dollar company.

However, those hopes were recently dashed, as Project Titan was canceled and the R&D team disbursed.

…And Outsourcing AI Shows Lack Of Vision

To add insult to injury, Apple appears to be conceding in the Generative AI arena before the race has even begun, as Apple is rumored to be negotiating with Google to allow Gemini AI to power Apple’s AI features.

In short, Apple appears to be following in Microsoft’s footsteps by missing out / giving up on new technologies that will shape the next decade of consumer technology spending.

Premium Valuation No Longer Justified

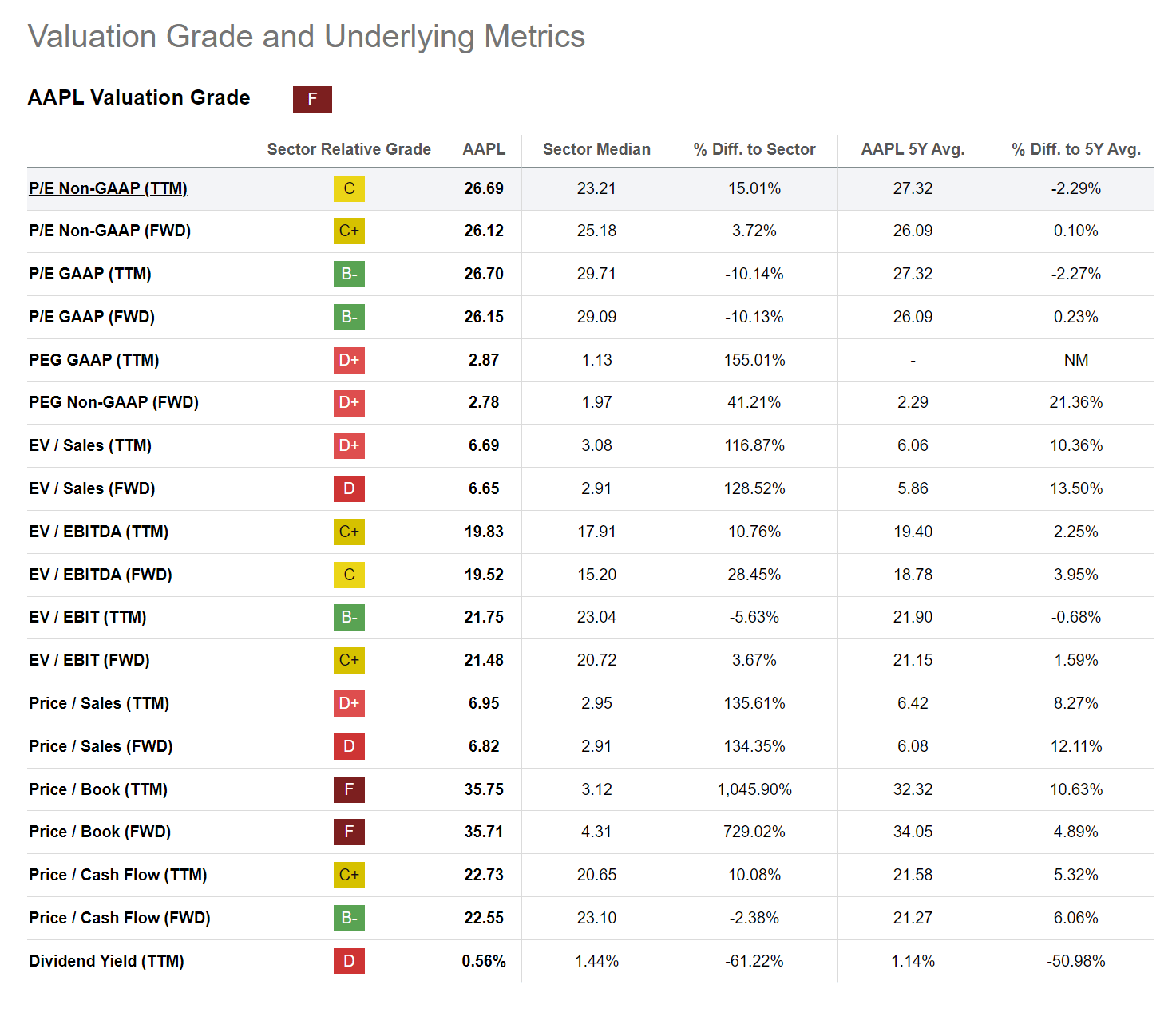

For a technology company giving up on growth, I believe Apple’s premium valuation is no longer justified. The company is currently trading at a forward P/E multiple of 26.1x with a negative trailing 12-month growth compared to 23.2x P/E for the S&P 500 (Figure 6).

Figure 6 – Apple valuation (Seeking Alpha)

{kind=link}

Buffett In Agreement With Sell

In fact, I am not the only one who believes Apple is overvalued here. The Oracle of Omaha, Warren Buffett, sold $2 billion of his Apple stake in Q4 2023. Mr. Buffett is a famously patient investor and does not like to sell shares unless there is a fundamental reason prompting him to do so.

All eyes will be on the upcoming Q1/2024 13F reports to see if Mr. Buffett simply sold enough Apple shares to offset 2023 realized losses in his portfolio or if he has really soured on the company.

Risk To Being Cautious

The biggest risk to being cautious on Apple is that a rising tide lifts all boats. As the U.S. equity markets appear to be in a strong bull market, even if Apple shares underperform, they should still appreciate with the market.

Furthermore, the rumored agreement with Google on Gemini AI may bring new revenue streams to Apple and boost its moribund growth rate.

However, I believe investors holding Apple for its growth should look elsewhere. Clearly, the company is suffering from the law of large numbers and has run out of ideas on how to grow its earnings, besides using financial engineering to buy back shares.

Conclusion

There is no question Apple has been an amazing company, rising from near death in the early 2000s to become one of the most valuable companies in the world with over $2.5 trillion in market cap. However, the key phrase is “has been.” I believe Apple’s best days are behind it, as the company has all the hallmarks of being past its prime and losing focus, with the company conceding on promising areas of growth like autonomous vehicles and generative AI.

While Apple’s shares may yet appreciate along with the market, I believe the company is a relative sell. Growth investors should look to sell their Apple shares and reallocate to other companies driving the next leg of growth in technology spending.